Key takeaways:

- Yields are not just pricing inflation volatility, but increasingly the return of fiscal risk, sovereign supply concerns, diminished central bank balance sheet support, and the re-emergence of the term premium as a meaningful market force.

- Central banks are more likely to keep policy restrictive against inflation persistence, continue balance sheet reduction, and in some cases, step away from acting as a backstop for long-end sovereign markets.

- A regime of structurally higher sovereign term premia challenges many of the assumptions underpinning traditional multi-asset portfolios, particularly the reliability of duration as a ballast, prompting a rethink of traditional asset allocation leaving investors to dig deeper for diversification.

Bottom line up top

Bond markets are selling off for valid reasons but drawing the wrong conclusions. An inflation shock, fiscal uncertainty, and central bank tightening are the familiar ingredients. What is building beneath them is more consequential, and harder to reverse.

The Pressure Markets Can See

Energy prices have surged, supply disruptions are feeding into headline inflation, and markets are repricing central bank tightening with growing conviction. Hints of fiscal stimulus to offset higher household energy costs are adding to the pressure, with bond yields testing multi-decade highs and the path of least resistance leaning higher.

Three variables may determine when that tactical pressure begins to ease:

- The trajectory of the Iran conflict, where any credible sign of resolution could rapidly unwind front-end rate pricing.

- Hard economic data validating the growth slowdown already evident beneath headline resilience.

- The pace of global oil inventory drawdowns, with April’s record decline illustrating how quickly the supply buffer is eroding, a harbinger of an acute growth shock.

But even if all three shift favorably towards bond bulls, the broader repricing story may not disappear with them. The inflation component of the current yield rise will eventually respond to demand destruction and tighter policy – but recent developments add conviction to the structural floor emerging for global bond yields.

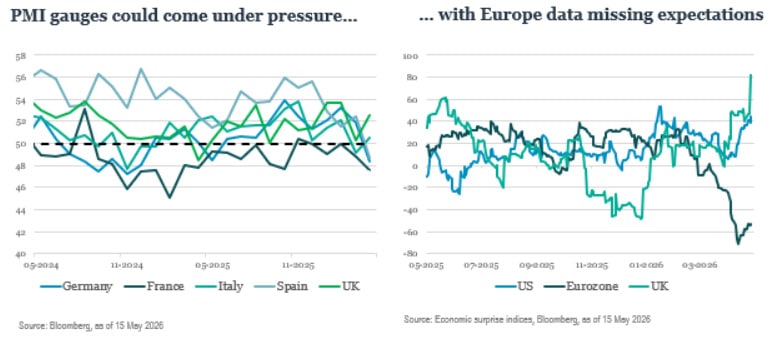

The Growth Mirage

The resilient growth narrative supporting risk appetite deserves greater scrutiny. Manufacturing PMI strength has been concentrated in backlogs of orders, supplier delivery times, and prices paid – signals of front-loading, inventory building, and supply anxiety rather than demand resilience.

Commodity markets are already reflecting this dynamic. Urea prices have doubled, Indonesia’s coal export volumes have surged roughly 40% quarter-on-quarter as economies pivot from oil & gas, and Chinese fertiliser plants are reverting to coal-based processes not used in years. These are signs of hedging behaviour and supply stress, not robust end demand.

Production and employment PMI sub-components are also weakening across both Europe and the US even as headline indices remain relatively firm. The greater risk is not the initial energy shock itself, but the persistence of second-round effects feeding through transport, utilities, and wage dynamics while underlying growth momentum softens beneath the surface.

That leaves central banks to face a growing risk of tightening into a slowdown, while any additional fiscal support will arrive at exactly the wrong moment in the monetary cycle.

The Fiscal-Monetary Collision

In prior cycles, fiscal expansion arrived when central banks had room to accommodate it, suppressing yields through balance sheet expansion and absorbing additional sovereign issuance. Monetary policy was doing the heavy lifting, keeping term premium compressed even as deficits widened.

That backstop is now being challenged. Central banks are more likely to keep policy restrictive against inflation persistence, continue balance sheet reduction, and in some cases, explicitly step away from acting as a backstop for long-end sovereign markets.

At the same time, households are increasingly squeezed, resilient corporate margins are at risk, and governments are likely to lean more heavily on fiscal support to cushion the cost-of-living crunch. But there is limited capacity for bond markets to absorb the spending at current yield levels without demanding additional compensation.

A Sovereign Universe That Is Fracturing

The yield moves have been broadly uniform across major developed markets, but the fiscal fundamentals underpinning it have not. That divergence is where the key investment implications increasingly reside.

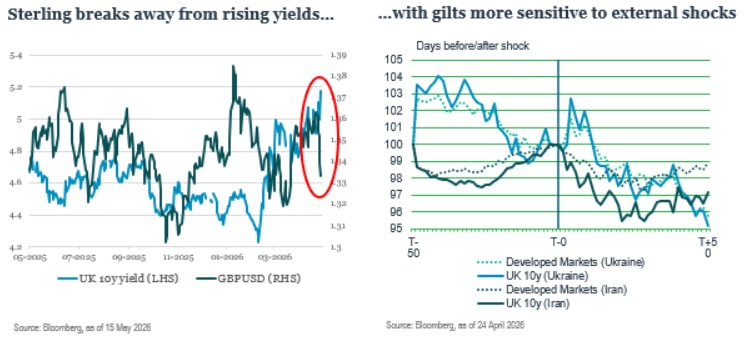

UK: Fiscal credibility under pressure

The U.K. remains the clearest example of the new regime, with gilts increasingly reflecting fiscal and political credibility rather than purely domestic growth fundamentals. The move higher in yields has been exacerbated by rising global inflation concerns, energy sensitivity, and renewed political uncertainty – all against the backdrop of a structurally shrinking long-end buyer base.

There is a growing risk of looser fiscal discipline under leadership uncertainty, though bond markets are likely to keep government spending ambitions in check. Gilt moves have likely already eroded more than half of the fiscal headroom outlined in the Spring statement, leaving limited cushion.

While we continue to see 10 yields moving back below 4.5% later this year as markets begin to price a cutting cycle – a cyclical late-2026 story – gilts are likely to remain under pressure from an embedded fiscal risk premium, elevated supply expectations, and structurally weaker demand for duration.

Europe: Insurance hikes into weakening growth

The ECB may embark on “insurance” hikes this summer, with inflation projections rather than spot inflation remaining the key anchor for policymakers. At the same time, Europe is likely to see modest fiscal support, with Germany retaining some capacity to cushion energy-intensive industries.

The greater risk is that policymakers respond to supply-driven inflation persistence by tightening into weakening demand conditions, creating the setup for deeper easing further down the line. Markets may still be underpricing that eventual growth deterioration, particularly if softer services data begins to confirm the slowdown already emerging beneath headline resilience.

We see opportunities in fading the third hike now priced, with softer services data acting as the trigger for covering European duration underweights.

US: A fiscal-led floor on yields

Our year-end forecast for the 10-year yield remains at 4.10% percent. Barring a prolonged geopolitical escalation, moderating services inflation and fading tariff effects should gradually pull core inflation lower by year-end, providing the Fed with scope for one rate reduction – though that remains a minority market view.

But even if the front end reprices lower, the long-end is likely to remain constrained by ballooning fiscal deficits and a structurally higher term premium environment, keeping curve steepening pressures intact.

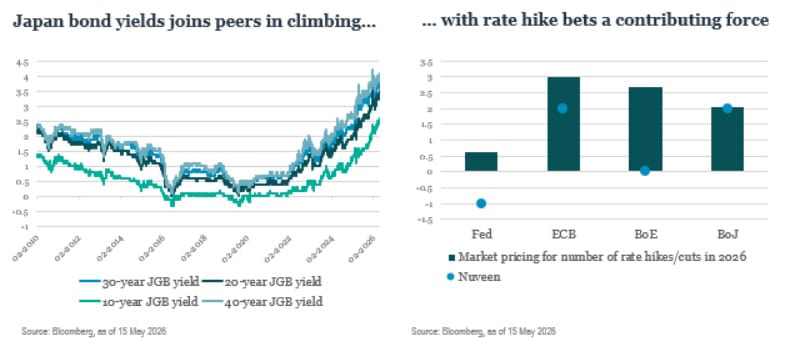

Japan: The anchor is shifting

Japan presents the most consequential structural shift for global bond markets. As the Bank of Japan gradually normalises policy, the largest suppressor of global term premia is slowly retreating.

While domestic investors are beginning to re-engage with JGB yields at multi-decade highs, as captured in a strong month of bond buying in March, the process should remain gradual and contingent on domestic confidence. Once the end of the hiking cycle is clearly signaled and greater clarity on the fiscal outlook emerges, locals are likely to return, and that is the catalyst we are watching for. Until then, the flattening trade remains more carry and roll-down than a directional bet.

While the moves started as a Bank of Japan normalisation story, the gradual removal of extraordinary policy accommodation is allowing the term premium to reprice toward levels more consistent with a regime of positive nominal growth and modest inflation. We see this as a healthy normalisation rather than a disorderly repricing, capturing a structurally higher yield backdrop.

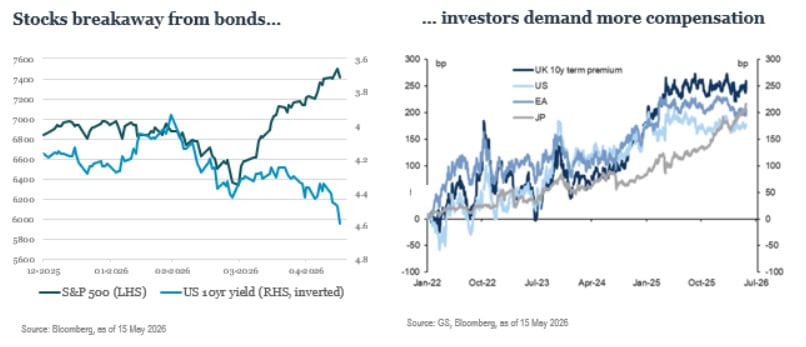

Bottom line: Higher for longer, for even longer

Yields are not just pricing inflation volatility, but increasingly the return of fiscal risk, sovereign supply concerns, diminished central bank balance sheet support, and the re-emergence of the term premium as a meaningful market force.

A regime of structurally higher sovereign term premia challenges many of the assumptions underpinning traditional multi-asset portfolios, particularly the reliability of duration as a ballast, prompting a rethink of traditional asset allocation leaving investors to dig deeper for diversification. While the energy shock will eventually resolve, the regime shift and portfolio implications it has accelerated will not.

")

Platform To Digitally Trade Corporate Bonds")