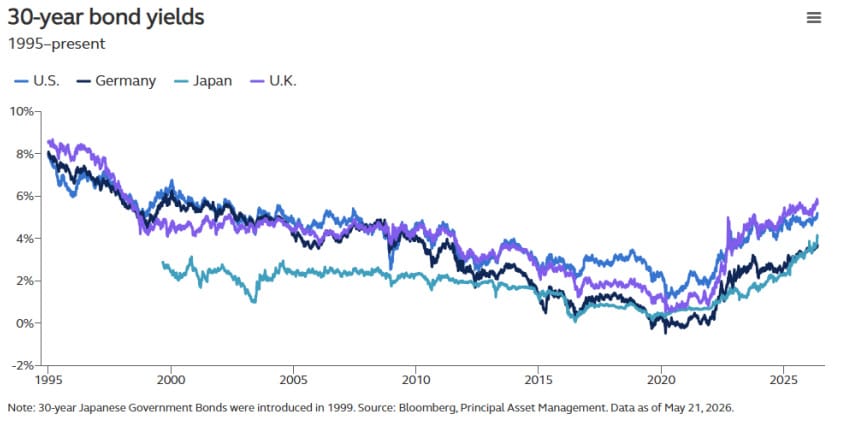

Global bond markets have sold off sharply in recent weeks, pushing long-end yields to multi-decade highs across major markets. U.S. 30-year yields hit their highest level since 2007, 30-year JGBs since their introduction in 1999, UK gilts since 1997, and German bunds since 2011.

This is not a series of isolated market moves. Rather, global bond markets are repricing a shared set of risks: stickier inflation, expansionary fiscal policy, and elevated geopolitical uncertainty with a prolonged closure of the Strait of Hormuz. Together, these forces, further reinforced by strong U.S. growth, are eroding confidence in the path towards policy easing and pushing yields higher globally.

Key market drivers

Rising inflation pressures

Higher energy prices are beginning to feed through into inflation. Headline U.S. CPI is running near 4% and producer price inflation near 6%, while rising freight costs suggest pipeline pressures have yet to peak. Importantly, although longer-term U.S. inflation expectations remain broadly anchored, early signs of strain are emerging. By contrast, inflation expectations in both Europe and the UK have already increased sharply.

Resilient U.S. growth

Growth remains robust. Consumer spending continues to hold up despite higher energy costs, while the capex cycle—supported in part by AI-related investment—continues to surprise to the upside. This resilience allows U.S. inflationary pressures to persist, sustaining upward pressure on yields.

Hawkish repricing of policy expectations

Markets have materially revised their outlook for central banks, shifting from expected rate cuts in 2026 to renewed tightening across several developed markets. In the U.S, stronger inflation data alongside firm growth has driven a significant shift in Fed expectations, with markets now assigning a material probability to a rate hike by year-end.

Fiscal concerns and rising term premia

Governments, including the U.S, are considering additional fiscal support to cushion the energy shock despite already stretched fiscal positions. This is contributing to higher term premia and reinforcing upward pressure on long-end yields.

Geopolitical risk premium

Markets are increasingly pricing in a prolonged Middle East conflict. The risk of sustained disruption to energy supply is embedding an additional geopolitical risk premium into yields.

Idiosyncratic factors

Local market dynamics, such as renewed UK political uncertainty over the possibility that Prime Minister Keir Starmer could be replaced by year-end, are adding to volatility.1

What could trigger a sustained bond rally?

A sustained reversal in the sell-off likely requires one of two developments:

• A meaningful slowdown in growth, sufficient to re-anchor expectations for policy easing; or

• A de-escalation in the Middle East, involving a reopening of the Strait of Hormuz and normalisation of oil flows.

With many investors positioned for further yield increases, a decisive geopolitical de-escalation could trigger a sharp rally in bonds, pulling both yields and oil prices lower and supporting risk assets. By contrast, a growth-driven decline in yields would likely come alongside weaker risk appetite.

Implications for equity markets

Equities have, so far, absorbed the rise in yields without too much damage. However, investors are increasingly concerned that rates are approaching levels that could challenge valuations. That said, the relationship between yields and equities is more nuanced than a simple “threshold” effect:

• The driver of yields matters: When yields rise on the back of stronger growth, equities tend to hold up well as earnings expectations improve. By contrast, supply-driven inflation, particularly via energy, pushes yields higher while compressing valuations, creating a more difficult backdrop for equities.

• The pace of the move matters: Even growth-driven increases can unsettle markets if they are too rapid.

Equities currently remain supported by strong earnings momentum. Global earnings-per-share expectations have been revised higher since the onset of the U.S./Iran conflict, reflecting continued strength in U.S. earnings and greater resilience in Europe than initially feared. This earnings cushion has so far enabled equities to absorb higher yields, contributing to the recent divergence between bonds and equities.

Looking ahead, U.S. equities should remain relatively resilient to rising rates, supported by strong earnings, the AI-led capex cycle, and lower direct exposure to higher energy costs. In Europe, by contrast, greater sensitivity to energy prices and weaker earnings momentum outside the energy sector leave equities more vulnerable to stagflation. That said, U.S. resilience should not be taken for granted: a further rise in energy prices—especially if it weakens growth and triggers a more hawkish Fed response—would put that relative strength to the test.

Investment considerations

Equities have so far been insulated from rising yields by strong earnings. However, the balance of risks is becoming increasingly finely poised, as higher rates, persistent inflation, and geopolitical uncertainty are beginning to challenge the durability of that support.

From a portfolio perspective, this environment argues for maintaining a more balanced and flexible stance:

• Stay selective in equities, favouring regions, sectors, and, importantly, companies with strong earnings visibility and pricing power, particularly those less exposed to energy shocks.

• Rebuild duration gradually, recognising that while near-term risks remain skewed to higher yields, higher starting yields are improving the medium-term case for bonds.

• Maintain exposure to inflation and geopolitical hedges, including energy and commodities, given the persistence of supply-side risks.

• Preserve optionality, as elevated uncertainty increases the likelihood of sharp, event-driven reversals across both rates and risk assets.

In this environment, portfolio resilience, rather than directional conviction, remains paramount.

1. Barclays Research, “Middle East disruption also exposes a tail risk to semiconductors.”

")

Platform To Digitally Trade Corporate Bonds")