Since the outbreak of the Iran conflict, market losses have been limited, at least so far. But it might not take much in terms of adverse developments in the Middle East to wipe out any remaining positive year-to-date returns. Patience and defensiveness tend to point to cash, short-duration and inflation-linked assets as a viable tactical stance until the fog of war clears.

- Key macro themes – We await more material changes to economic and central bank forecasts

- Key market themes – Volatility driven by headlines but no obvious market ‘cheapness’

A spectrum of outcomes

Investors continue to face the risk that the Middle East conflict might (re)escalate further. Recent developments, however, have also suggested a ceasefire is possible, which would bring some relief to oil markets.

While markets have been disrupted significantly in recent weeks, drawdowns have largely stopped short of major corrections. Of the major equity markets, only the Korean KOSPI and the MSCI Emerging Markets indices have corrected by more than 10% from their recent highs.

There also remains a scenario in which markets must price in a tightening of monetary policy as central banks lean against higher short-term inflation becoming embedded in expectations.

However, the interest rate path is unclear, and arguably, markets have done quite a bit of tightening for central banks already. Since the conflict began bond yields have moved higher, while equity markets are materially lower.

Confidence in any scenario in the coming days and weeks is necessarily low. This provides a significant challenge to making investment decisions. The timing and characteristics of the optimal exit point are unknown.

Value hunting

Have markets moved enough to reveal value opportunities? Inflation is going to move higher. That is a given. But rates are and the inflation tailwinds have been more favourable. In a de-escalation scenario, oil prices should ease and, although energy costs overall will remain elevated, the pass-through to consumer prices might be modest in terms of size and duration.

It is hard to make the case that rates will rise more than is currently priced in. Add on a 15 to 20 basis point widening in credit spreads since 27 February, and short-duration investment grade credit does look attractive – high yield potentially even more.

Investors may also want to look at floating rate instruments in this environment. In addition, higher consumer price indices will boost returns from short-duration inflation-linked bond strategies in the coming months.

Little is cheap

The broader view is that a limited number of assets have materially cheapened, but they tend to be those that responded to concerns around artificial intelligence disruption or private credit concerns before Iran rather than the conflict itself.

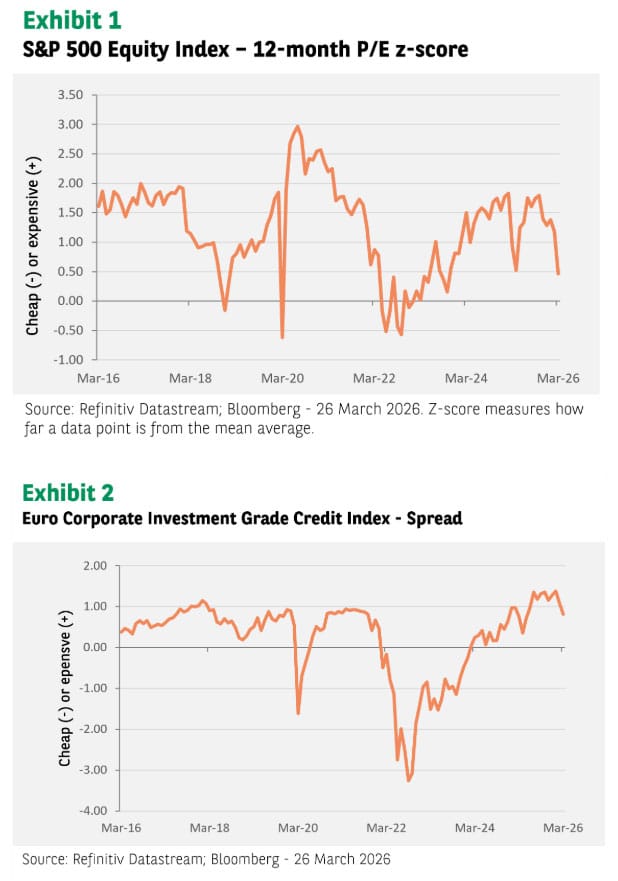

I looked at where 12-month price-to-earnings ratios for equities, and option-adjusted spreads for credit, stand after more than three weeks of conflict relative to their averages of the last three years.

Asset classes which have cheapened the most since the start of the year (relative to their three-year average) include the Nasdaq and S&P 500 indices – notably the Information Technology and Financials sectors of the latter index as well as the global MSCI Emerging Markets equity index. European and US high yield indices are also cheaper because of higher spreads.

Taking a longer-term view, however, it is difficult to see any real market ‘cheapness’. The Nasdaq, US small caps, and global emerging markets are trading on P/E ratios just below their 10-year averages. Other equity markets, including the S&P 500, remain at a premium to longer-term valuation metrics.

On the metric used here, Europe, the UK and Japan were much cheaper in 2022. In credit, spreads are still well below their 10-year average levels, except for the small technology and electronics sector of the US high yield market. So, while most markets are lower, in fixed income the real shift in value has been the rise in underlying rates curves. The real (inflation adjusted) US 10-year Treasury rate is back above 2.0% for the first time since mid-2025.

Risk premiums have risen but not by enough to compensate investors for the still possible very adverse scenario in the Middle East.

Defence is the best form of attack

It is a challenging time to manage portfolios. There is an incentive to hold more cash and cash-like assets, and those that offer inflation protection. Economists are starting to revise down growth forecasts but material revisions to equity earnings forecasts have not happened yet.

The risk is that, as we get more corporate guidance around the first quarter earnings season, growth forecasts will be lowered. That is the risk for equities, while the ongoing flow of negative headlines around private credit might, at some point, infect the public credit markets.

A scenario of higher equity volatility, lower equity prices and wider credit spreads cannot be ruled out, conditional on how things evolve in the Gulf. Having cash-like liquidity can be an advantage in such circumstances.

Being patient is a virtue and a necessity for longer-term investors. Gradually locking in higher risk premiums without betting on a rapid return of market prices to pre-conflict levels seems a sensible approach.

Headline risk remains high, shifts in sentiment are binary, depending on fluctuations in the price of Brent crude. A cessation of hostilities is the very minimum that investors should require before there is more confidence in committing capital to higher return assets.

Performance data/data sources: LSEG Workspace DataStream, ICE Data Services, Bloomberg, BNP Paribas AM, as of 26 March 2026, unless otherwise stated).

Platform To Digitally Trade Corporate Bonds")