Thomas Poullaouec, Head of Multi-Asset Solutions APAC at T. Rowe Price, and his team have published their latest insights on global asset allocation and the investment environment for Australia. February 2026.

OUTLOOK

Ongoing geopolitical conflict and a more pronounced energy supply shock leading to higher inflation and rates could challenge risk assets, with valuations remaining somewhat elevated. That said, earnings momentum and economic growth remain favorable, underpinned by accommodative fiscal policies across many regions.

U.S. economic growth continues to show resilience driven by AI-driven capex spending, consumer spending and supportive fiscal policy. However, weakness in the labor market warrants monitoring.

Markets outside the U.S. continue to benefit from firmer domestic demand and policy, particularly in Europe and Japan.

Economic activity in Australia remains resilient, with growth and employment above potential and elevated commodity prices a material positive. However, persistent inflation pressures reinforces the central bank’s shift to a more hawkish stance.

Key risks to global markets include escalating geopolitical tensions, a resurgence in inflation, reliance on AI-driven growth, further deterioration in labor markets, and a widening of liquidity concerns within private credit.

THEMES DRIVING POSITIONING

Drumbeat

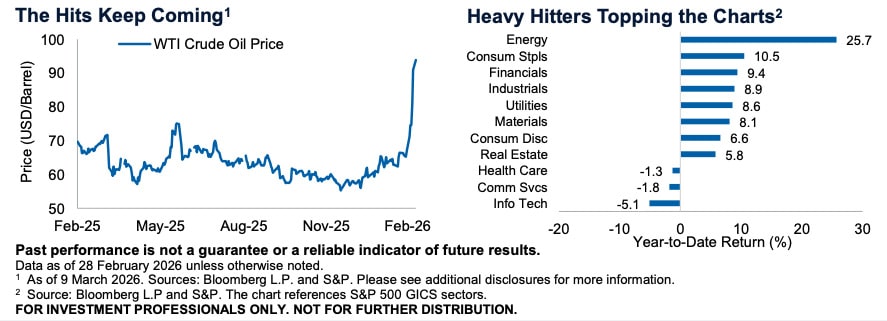

Equity markets have been rallying around expectations of stronger economic and earnings growth supported by fiscal spending this year. However, there has been an increasing drumbeat of negative headlines that may challenge that outlook. The latest being the US and Israeli attack on Iran which has led to a spike in energy prices, with no clear end in sight. This comes on the heels of rising concerns over AI, including the disruptive impacts on some business models and the magnitude and ultimate payoff of AI capex spending.

There has also been a notable rise in headlines surrounding private credit market liquidity and exposures to some vulnerable sectors of the market. And while we don’t see any

of these leading to a systemic risk today, the culmination, particularly as we move closer to mid-term elections and new leadership at the Fed, could lead to much louder drumbeats.

For now, we maintain hedges to some of these risks, particularly inflation, and will look to market volatility for opportunities given our still constructive view.

Also read: The Fed’s Dovish Hold

Heavy Metal

Markets have seen a notable shift in performance toward “asset-heavy” sectors, with the likes of natural resources, energy, utilities and defense companies coming into vogue.

Over recent weeks, investors have become increasingly concerned over the prospects for AI displacing certain business models, including software development and asset

management companies. And while the concerns initially sent investors into more asset-heavy sectors presumed to be less vulnerable to AI disruption, many of these companies

are actually seeing improving fundamentals. The expansion of AI and related infrastructure build is raising demand for energy, metals and materials, and global fiscal spending should also provide a boost. Notable changes to tax policy now allowing for accelerated expensing of capex could also drive increased demand within these sectors. So, while asset-lite companies, many of which are tech-related, have been the darlings for years, markets may be tuning into a new genre, with “heavy metals” making a comeback.

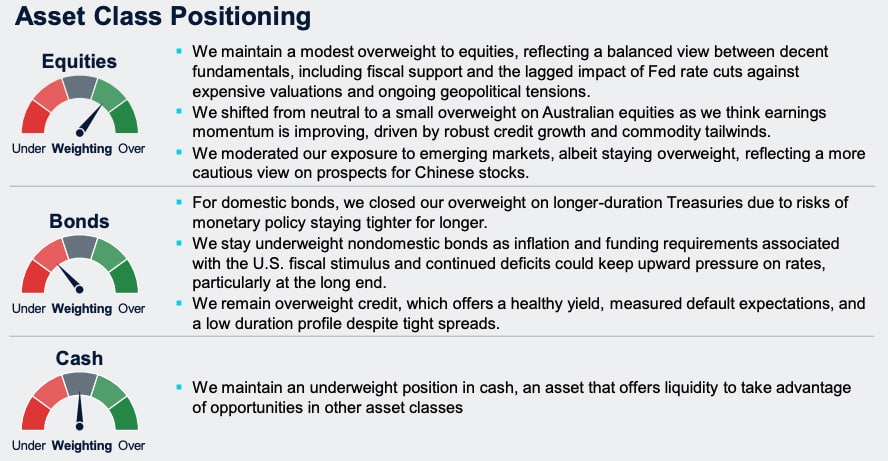

ASSET CLASS POSITIONING

Note: T. Rowe Price’s Australia Investment Committee comprises local and global investment professionals who apply views from the firm’s Global Asset Allocation Committee to make informed asset allocation views from an Australian investor perspective. The Committee is led by Thomas Poullaouec, Head of Multi-Asset Solutions APAC, based in Singapore.

")

Platform To Digitally Trade Corporate Bonds")