From Joe Unwin, Head of Portfolio Management at Apostle Funds Management

Private credit is in the media spotlight right now, but for the wrong reasons.

Frequent headlines about redemptions from retail funds and valuation write-downs paint the picture of an asset class with increasing risk.

However, there is limited evidence of broad-based deterioration in performance across the asset class.

Instead, these negative headlines suggest that some managers may have lowered their lending standards over time in order to compete for deals and grow their AUM.

By avoiding these portfolios and focusing on cycle-tested managers that have maintained their lending discipline, investors can still access attractive forward-looking risk-adjusted returns from private credit.

Which portfolios may be well-positioned?

In our view, increasing dispersion across private credit markets means manager selection and portfolio construction are becoming more important.

Private credit strategies with the following characteristics may offer compelling forward-looking risk-adjusted returns to investors:

- Core middle market focus – the core middle market – companies with EBITDA of $10-50m – is widely considered the sweet spot of direct lending. It has less competition for deals than the upper middle market, resulting in better pricing and stronger covenants/lender protection, whilst having arguably less risk than the lower middle market. Many strategies have ‘drifted’ into the upper middle market to support AUM growth. Managers that have remained focused in the core middle market segment are likely to offer more attractive risk-adjusted yields.

- Minimal exposure to PIK interest – More than 11% of US middle market loans used payment-in-kind (PIK) interest as at Q4 2025 according to Lincoln International – a figure that has more than doubled since the start of 2022. Some advocates have defended this number, arguing that PIK can be a positive deal feature. However, 6.4% of loans used ‘bad PIK’ – that is, PIK that was not part of the original structure but was introduced later to defer interest payments. ‘Bad PIK’ may indicate that a borrower is unable to meet scheduled interest payments and is widely viewed as a credit red flag. Low PIK exposure is typically a sign of stronger lending discipline, while elevated levels may indicate emerging credit stress in a portfolio.

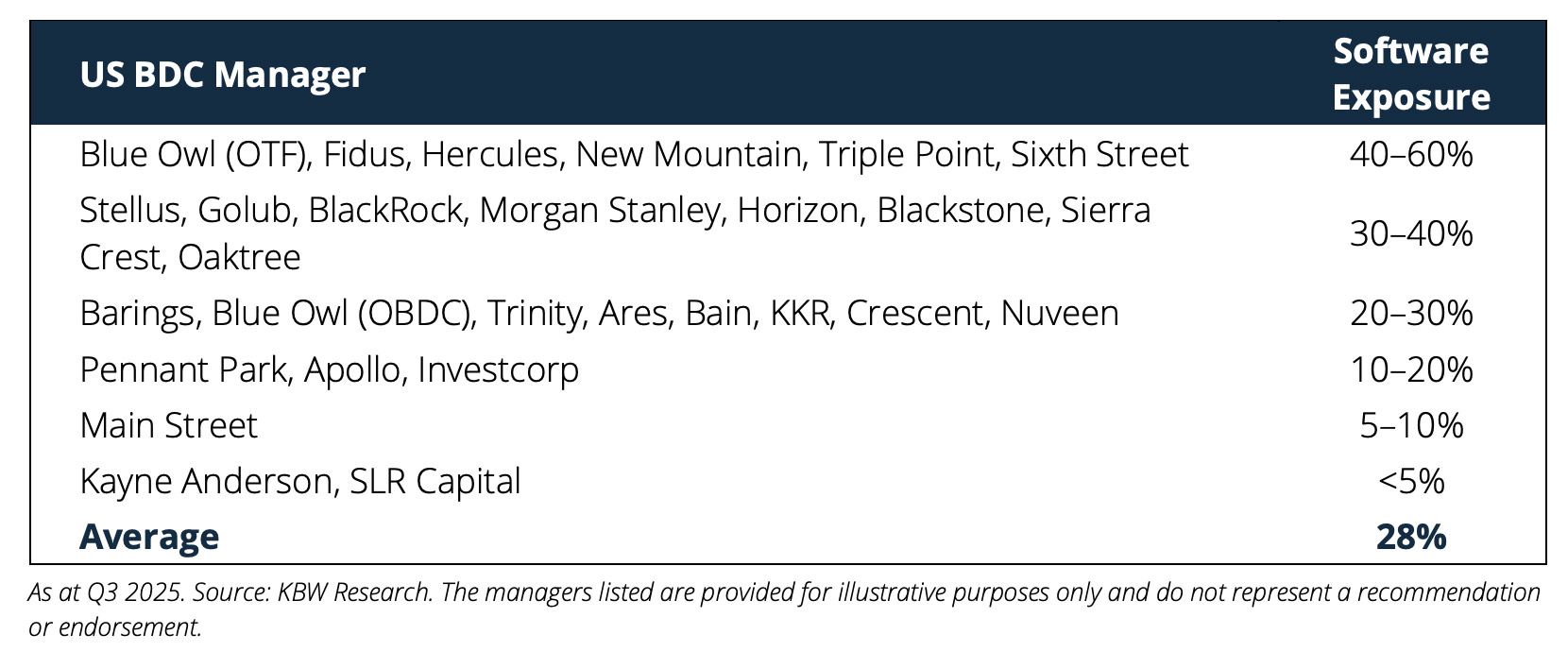

- Avoid concentrated sector exposures (e.g. software) – recent headlines have highlighted the fact that many private credit managers have built large, concentrated exposures to the software sector, including an average exposure of 28% amongst listed BDCs. An exposure of that size to any sector can reflect poor risk management practices and may be a result of larger managers needing to deploy excess capital in sectors with higher demand for leverage. Investors can mitigate this risk by identifying managers whose portfolios are well diversified across sectors. Concentrated exposures to the software sector are particularly concerning given several characteristics that are less suited to credit investors, including high valuations, reliance on growth, limited hard assets and sensitivity to technological disruption.The dispersion in software exposure across listed BDCs highlights how significantly manager positioning can vary.

Overall, current market conditions are reinforcing a key feature of private credit: dispersion between managers is widening.

Overall, current market conditions are reinforcing a key feature of private credit: dispersion between managers is widening.

While parts of the market are showing signs of weaker underwriting and increased risk tolerance, disciplined managers with consistent lending standards and portfolio construction frameworks continue to demonstrate resilience.

For investors, this environment is less about the asset class itself and more about selecting the right exposure – focusing on managers with established credit processes, conservative structuring and experience navigating more challenging conditions.

")

Platform To Digitally Trade Corporate Bonds")