Thomas Poullaouec, Head of Global Investment Solutions, International and Portfolio Manager at T. Rowe Price, and his team have published their latest insights on global asset allocation and the investment environment for Australia. May 2026.

OUTLOOK

Markets have remained largely resilient despite ongoing geopolitical tensions continuing to threaten higher inflation and weigh on growth, leading us to make some rotations in our regional equity exposures.

The global economy continues to show pockets of resilience, supported by a steady consumer, fiscal spending, and ongoing investment, particularly in AI, though growth is moderating and becoming more uneven across regions.

For Australia, energy supply risks and higher fuel prices continue to raise domestic inflation risks, while consumer and business confidence indicators have weakened.

Monetary policy remains steady with central banks largely in a holding pattern as they assess the path of inflation, while near-term inflation pressures persist in some areas, longer-term expectations remain relatively contained.

Key risks include a further escalation in geopolitical tensions, renewed inflationary pressures, greater reliance on a narrow set of growth drivers, potential labor market deterioration, and emerging liquidity concerns in parts of private markets.

THEMES DRIVING POSITIONING

America’s Market Moat

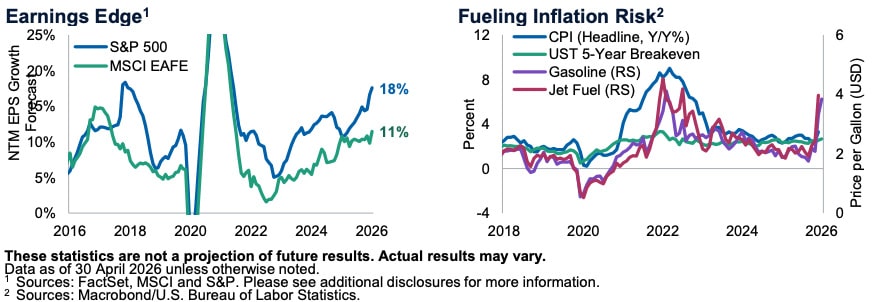

We re-initiated an overweight on U.S. equity as stronger earnings momentum, economic resilience reinforced by AI leadership, better energy insulation, and supportive fiscal policy improve the relative case. Earnings revisions are accelerating more quickly in the U.S., with EPS growth expected to reach its strongest pace since the COVID-19 rebound. AI leadership remains U.S.-centered, but its depth extends beyond semiconductor demand and into power generation, data center construction, supporting infrastructure, and broader capital goods, strengthening the domestic capital spending backdrop. The U.S. is also better insulated from a Strait of Hormuz shipping disruption, given its status as an energy exporter and lower risk of shortages relative to Europe, Australia, and parts of Asia. Fiscal policy, including measures under the “One Big Beautiful Bill,” should continue to support domestic demand. While non-U.S. equities benefit from cheaper valuations and increased defense spending, the U.S. “moat” of stronger earnings momentum, AI leadership, energy insulation, and policy support is increasingly compelling.

Also read: Private Credit Headwinds Move Onshore

Blind Spot

Inflation risks represent a potential market blind spot, given uncertainty around the persistence of the energy supply shock. Two months into a near-complete shutdown of the Strait of Hormuz, oil movement remains severely disrupted, creating regional shortages and broader price pressures reflected in gasoline, jet fuel prices, and utility bills, which feed through to consumers and businesses. Gulf states are also major fertilizer suppliers; shortages could add another layer of pressure through higher food prices. While markets are hopeful for a quick resolution, oil flows may still take several months to return to pre-war levels, suggesting this shock may not fade quickly. At the same time, energy, defense and infrastructure spending, as well as AI-related demand for more power, data centers, equipment and labor are additional inflationary forces in the U.S. Despite these risks, longer-term inflation expectations remain in line with pre-war trends. Barring a recession, inflation prints could surprise higher and weigh on activity. Against this backdrop, we have increased our inflation protection positioning.

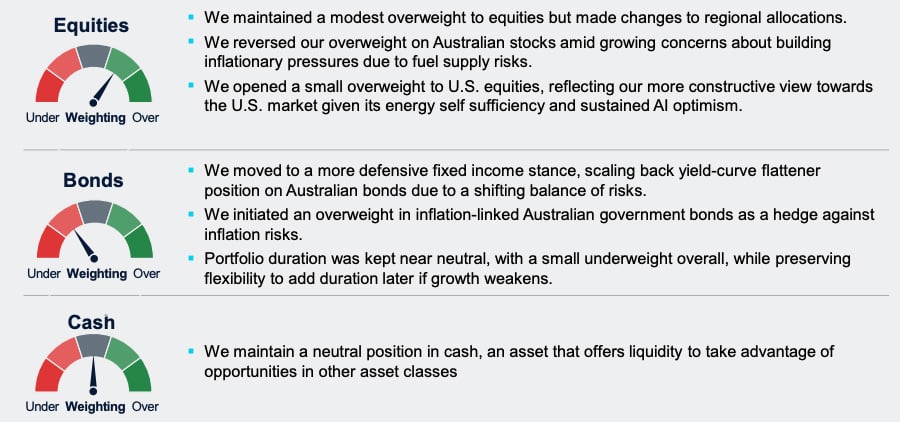

ASSET CLASS POSITIONING

ASSET CLASS POSITIONING

Note: T. Rowe Price’s Australia Investment Committee comprises local and global investment professionals who apply views from the firm’s Global Asset Allocation Committee to make informed asset allocation views from an Australian investor perspective. The Committee is led by Thomas Poullaouec, Head of Multi-Asset Solutions APAC, based in Singapore.

")

Platform To Digitally Trade Corporate Bonds")