By Gregory Peters, Co-Chief Investment Officer, Public and Private Fixed Income, PGIM

Bonds continued to navigate economic uncertainty in 2025, extending their impressive bull market. With a stable economy and the US Federal Reserve poised for rate cuts, conditions remain favourable for fixed-income assets. Attractive yields offering steady income have been largely responsible for progress since the 2022 selloff, rather than gains from capital appreciation. The market’s steady course highlights what can aptly be called a “carry market,” where income streams continue to support returns, albeit with a likely boost from Fed rate cuts.

Stuck in the muddle

Global economy: Despite uneven economic conditions and lingering recession concerns, we believe developed markets point to a “muddle through” future marked by low-to-moderate growth and mildly sticky inflation.

Short-term interest rates: Continued Fed rate cuts toward a neutral target range of 3.00%–3.25% hinges on two major developments: A shift in Fed policy: A potentially more dovish Fed, particularly when Chair Powell’s term ends in May 2026, could result in a lower, steeper yield curve.

A weakening job market: A softening U.S. labor market, which prompts further Fed easing, could spark a short-to-intermediate term bond rally, even as long-term inflation risks persist.

Long-term interest rates: Long yields in the U.S. appear to have passed their peak, a bullish signal for Western markets, where U.S. trends heavily influence cross-market correlations. We expect U.S. rates to remain range-bound, with the 10-year yield drifting between 3.95-4.20%, creating tactical opportunities at the edges of the range.

The long end of the U.S. yield curve also remains susceptible to an “overheating” economic scenario, including another lift in inflation where the Fed is compelled to cut rates below the estimated neutral level. Capitalising on credit spread dynamics Excluding tariff-related volatility earlier in the year, spreads remained within a tight range in 2025. Looking ahead, spreads are expected to stay range-bound with occasional periods of widening. Currently near the lower end of their range, spreads call for caution, reducing risk as spreads tighten and selectively adding exposure when they widen.

Also read: Investment Themes for 2026

Navigating the bond bull market in 2026

Money market assets remain near record levels, representing a massive potential source of demand for stocks and fixed income, particularly as falling cash rates incentivise a shift out of money markets. Rising geopolitical risks and potential market volatility further support the case for greater bond exposure.

Prepare for rate volatility: Given a Fed pivot could send yields in either direction, balancing short-dated securities with select intermediate-to-long maturities seems prudent.

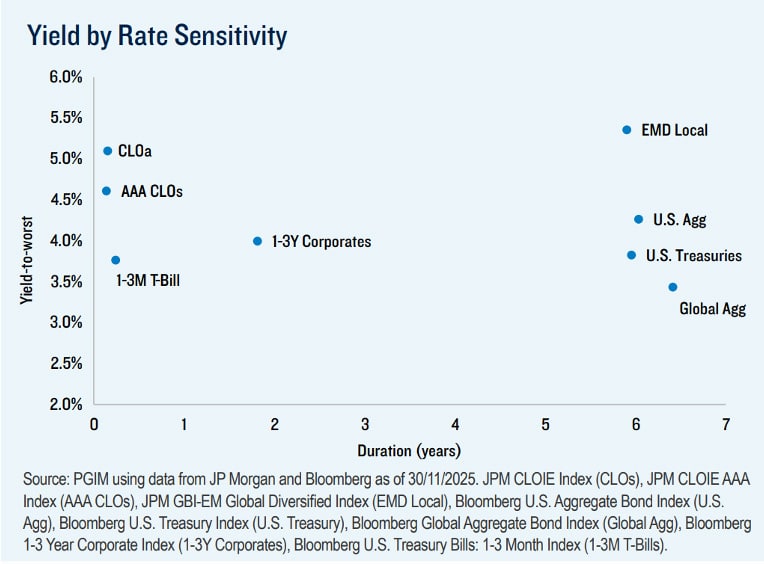

Go global: As uncertainty around U.S. inflation and indebtedness may rise, consider other developed sovereign bonds to mitigate U.S.-specific risks. Emerging market debt, especially in local currency, continues to offer diversification and attractive carry.

Be selective: In an uncertain environment, positioning for a range of outcomes is critical. Active management and selectivity are key to unlocking opportunities in high quality credits and securitised assets like collateralised loan obligations.

Technical tailwinds for bonds

The current environment offers disciplined, tactical opportunities for active fixed income investors. By balancing short- and intermediate-duration strategies, remaining cautious on credit selection, and capitalising on technical tailwinds, investors can position effectively for an ongoing bond bull market.

")

Platform To Digitally Trade Corporate Bonds")