Capital Group has provided its mid-year outlook for fixed income investors

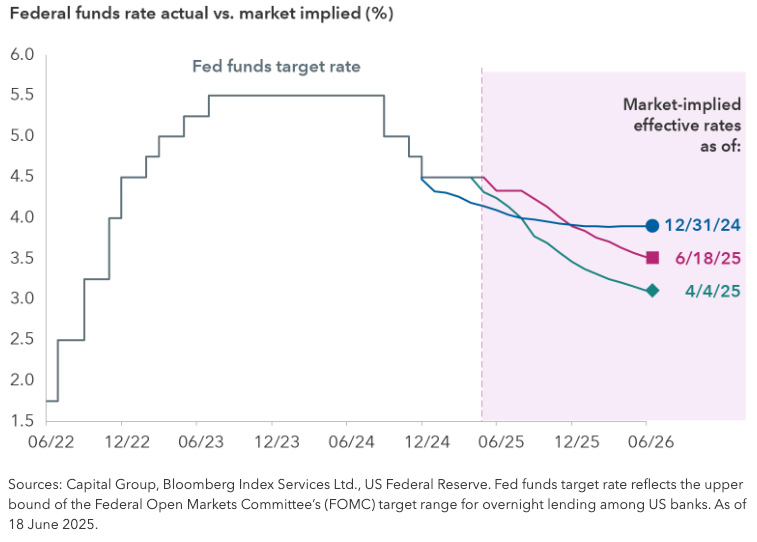

Fed: Market expectations for a near-term rate cut have softened, with the Fed consistently signaling a desire to be patient in assessing the growth and inflation effect of tariff policies. Interestingly, longer-term markets are expecting more rate cuts than they were at the start of the year – a mid-2026 cash rate of 3.5%, which implies ~1% of rate cuts (see chart below).

US Treasuries: This segment has seen elevated volatility as investors weigh concerns over higher inflation and lower growth, both stemming from tariffs; expectations of a growing US federal budget deficit have also weighed on markets. This is reflected in a view from our US rates analysts that there are multiple feasible scenarios which could cause yield curves to steepen.

More broadly US duration still plays a useful role in portfolios, offering valuable diversification even amidst elevated rates volatility. We saw this earlier in the year, where the S&P 500 fell 18.7% peak to trough (Feb 19 – Apr 8) and the US Agg gained 1%. Looking forward, importantly, the Fed has plenty of room to cut rates should economic conditions weaken more than expected, reinforcing the defensive ballast role of US duration.

Global rates: Germany’s fiscal pivot, EUR strength and trade uncertainty has reshaped the landscape for European rates. The net impact is likely disinflationary, which should make it easier for the ECB to cut rates more rapidly. In our view, the ECB is likely to err on the side of doing more rather than less to help ease upward pressure on the euro and to minimise the output loss from higher tariffs.

In Japan we have seen an extreme steepening in JGBs. The recent sell-off in the long-end has been driven by concerns of demand-supply imbalance – we think this dislocation is temporary and anticipate the BoJ will now pause hiking rates and potentially take measures to address the supply demand imbalance.

Also read: Emerging Market Debt Back in Focus for Australian Institutions

Credit: Healthy corporate fundamentals and attractive yields should help corporate investment-grade (BBB/Baa and above) and high-yield bonds weather potential headwinds to growth. Per Chit Purani, fixed income portfolio manager: “I currently favour an up in quality tilt toward credit exposures across bond sectors and issuers, as you’re not getting paid appropriately to take on riskier investments. The market has priced in a very optimistic outlook, and while recession is not my base case, it’s crucial for bond portfolios to serve as a ballast when volatility hits.”

Exposure to securitised assets including agency mortgage-backed securities (MBS) could benefit portfolios given their higher quality and attractive nominal yields and spreads compared to corporate credit. Areas of securitised credit also look attractive – e.g. senior tranches of subprime ABS (shorter maturities, improved lending standards); some CMBS (focus on higher quality tranches) offer strong income with reasonable valuations. Selectivity is crucial.

EMD: Downward revisions to global growth, falling energy prices, and easing core inflation all point to a lower interest rate trajectory across emerging markets – potentially favourable for EM local currency bonds. “While the potential for a spike in risk aversion remains higher than normal with US foreign policy uncertainty, EM countries are in a relatively strong position to face any upcoming challenges, considering mostly solid fundamentals and supportive technical factors” (Kirstie Spence, fixed income portfolio manager).

Weather")

")

Platform To Digitally Trade Corporate Bonds")