By Michael Goosay, Principal Asset Management

Reflecting on 2025, investors have encountered uncertainty fuelled by tariffs, geopolitical conflicts in Europe and the Middle East, and the implications of the One Big Beautiful Bill. Yet, amidst these challenges, the U.S. economy displayed surprising resilience, supported by strong consumer spending and corporate profits, which ultimately laid the groundwork for positive market performance.

Looking ahead to 2026, the fixed income landscape presents a cautiously constructive backdrop. While inflation is expected to remain above the Fed’s 2% target for the foreseeable future, the central bank is likely to gradually adjust interest rates downward toward a neutral level, projected to be around 3%. Although achieving this target is a priority, the Fed will likely tolerate some inflation beyond this level without compromising price stability. Against this backdrop, the opportunity for attractive income and total return remains, especially for active investors prepared to navigate sector dispersion and policy nuance.

Macro dynamics supporting the outlook

The trajectory of the Fed’s policy will be crucial in defining the fixed income landscape in 2026. We expect the Fed to begin gradually lowering rates by mid-year as it seeks to balance persistent inflationary pressures with a cooling—but not collapsing—labor market. This gradual recalibration is essential for fostering sustained economic growth, even in the face of sticky but steady inflationary pressures. Market expectations already reflect a more accommodative approach to policy changes sooner than previously anticipated, as the Fed effectively balances its dual mandates of stable prices and full employment.

Yield curve and duration positioning

As the Fed moves to lower interest rates further, there is potential for a steeper curve, which is consistent with prior easing cycles. Such environments typically lead to appreciation across the yield curve, offering investors opportunities to capture gains alongside income generation.

We remain moderately long in duration, emphasizing flexibility to respond to curve shifts and evolving inflation expectations. Effectively managing exposure across both ends of the curve will be key to optimizing returns in this interest rate environment.

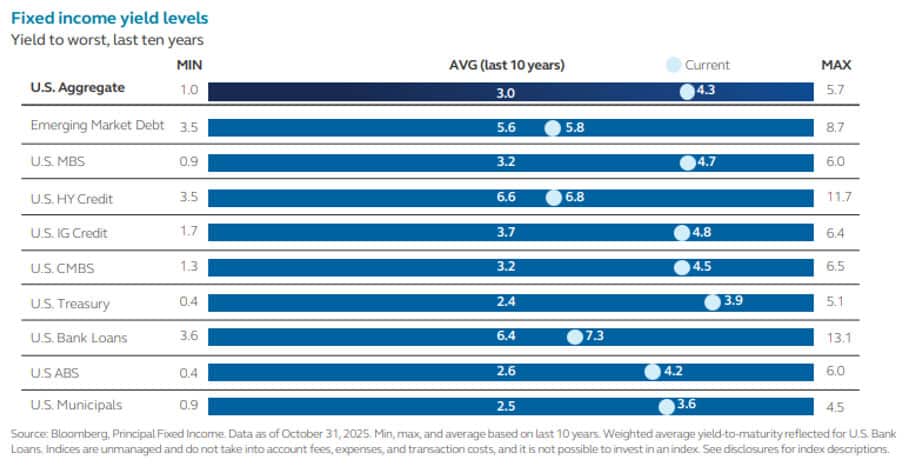

Sector views: Staying opportunistic and selective

High yield

High yield remains particularly attractive due to its limited potential for spread widening or further tightening. Despite economic uncertainty, the credit quality has improved markedly, with a reduction in the number of lower-rated issuers, which has helped tighten spreads. In fact, the percentage of CCC-rated securities fell to just 10% of the index, which justifies spread levels, and positions high yield as a compelling carry trade in a low-interest-rate context.

New issuance was heavy in 2025, and we expect that to continue. The market has easily absorbed this paper, but eventually the risk of supply exceeding demand will grow. So, while still overweight, we are biased toward a neutral position.

Investment grade

Investment grade credit continues to be viewed favourably, supported by strong technicals, solid fundamentals, and a favourable macro environment. However, tighter spreads present a more complicated landscape. Although demand for corporate debt and high-quality paper will likely persist, new supply may eventually outpace demand as firms take advantage of the Fed’s easing cycle to step up issuance. Moreover, consumer-linked credits may face challenges should the labor market weaken. Overall, IG credit remains resilient, allowing active managers to leverage bottom-up credit selection and sector differentiation effectively. Nevertheless, potential upticks in supply may weigh on the sector.

Emerging markets

Emerging markets present another area of interest, characterized by unique regional stories, opportunities and risks. With a positive outlook for certain segments driven by declining global rates, emerging market debt appears promising. But it is crucial for investors to focus on regional strengths and sector specific dynamics rather than adopting a blanket bullish approach. As an active manager, we seek to take advantage of individual markets, both dollar-denominated and local currency. Looking ahead, there are opportunities in the sector for an agile active manager, and we remain overweight.

Municipal bonds

Municipal bonds have underperformed other fixed income sectors through most of 2025, resulting in a very attractive risk/return profile, particularly on a tax-adjusted basis. Heading into next year, we’re in an environment where many coastal states, and parts of the Midwest are raising tax rates, and that’s likely to continue. That, in turn, should feed demand and drive attractive returns in the municipal bond space. Within Munis, we tend to avoid general obligation assets and focus more on revenue bonds and infrastructure projects where there are opportunities to extract value from an alpha perspective, while reducing risk.

A favourable outlook, but the ability to adapt is key

The fixed income market is characterized by a delicate interplay of factors that require careful navigation. Investors should remain vigilant regarding inflation trends and the Federal Reserve’s policy adjustments, as these will significantly influence the yield curve and sector performance. Yet this environment bodes well for fixed income investments. Investors can benefit from more favourable income rates compared to the ultra-low levels of a few years ago. This holds the potential for reasonable total returns in 2026.

Platform To Digitally Trade Corporate Bonds")