From Michael Goosay, An excerpt from Principal Asset Management’s 2Q 2026 Fixed Income Perspectives

The fixed income outlook is shaped primarily by geopolitical uncertainty— especially the conflict in Iran—which has driven volatile market behavior and elevated near-term risks to inflation. While the underlying economic backdrop entering 2026 was constructive, recent events have produced an erratic market: rates move sharply on news, while credit spreads reflect uncertainty about the implications for growth and inflation. Crude oil volatility has pushed net prices higher year-to-date, increasing the likelihood that headline inflation will drift upward over the next few quarters after a period of improvement. That, in turn, raises the real returns investors demand from fixed income, putting upward pressure on yields and steepening or repricing parts of the yield curve.

The central bank outlook is growing complicated

The earlier central bank divergence—where some central banks (e.g., Japan, Australia) were hiking while others (U.S., UK, Europe) were cutting—has given way to a more complex global picture: all central banks now face difficult choices about easing amid sticky inflation and macro uncertainty. Despite this, our view remains that the Federal Reserve will cut policy rates in 2026. With a new Fed Chair expected in June, the forecast is for one to two rate cuts in the second half of the year, driven by softer employment data and a tolerance for elevated inflation over time. However, near-term risks from geopolitical developments make the exact timing and magnitude of cuts uncertain.

Credit spreads are also mixed

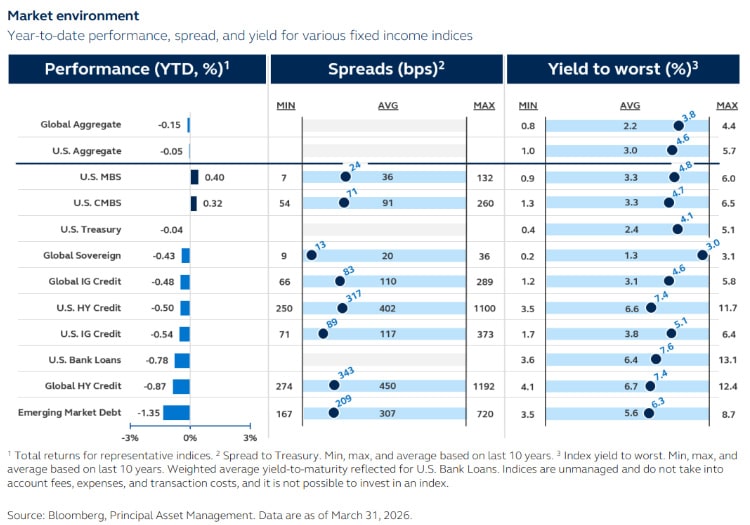

In credit, corporate fundamentals are generally solid—companies have sound balance sheets and earnings have generally beat expectations—so wider spreads are seen as opportunities for selective investment rather than signals of systemic weakness. Heavy supply has contributed to spread widening, and geopolitical uncertainty may keep upward pressure on spreads. Emerging market debt faces more pronounced stress due to a stronger U.S. dollar and capital flight into perceived safe-haven developed market assets. At the same time, investment grade credit shows only modest spread widening, while high yield shows more meaningful widening.

Fixed income investors are best served by taking risk selectively, guided by fundamentals and adding exposure only when market movements create genuinely attractive opportunities.

Also read: The Adverse and the Less-Adverse

Investment Implications

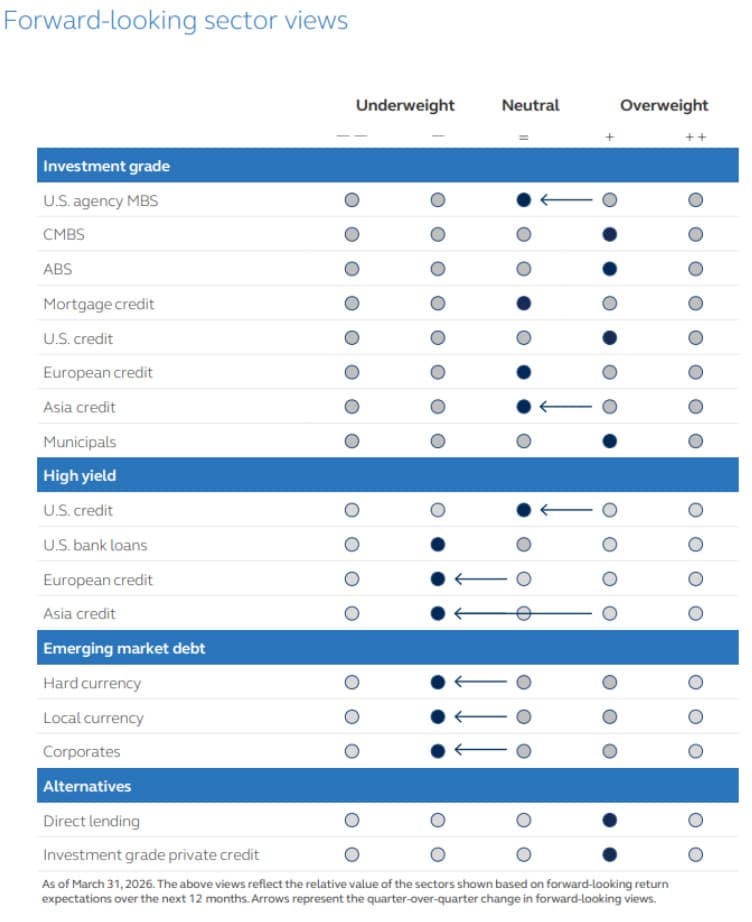

Investment Grade Credit

Investment grade credit appears able to absorb record issuance—now running ahead of forecasts—supported by robust investor demand. The 10-year Treasury remains the fulcrum for yields; with yields likely to stay around or above 4%, attractive carry and rolldown make the five- to ten-year belly of the curve the preferred allocation while keeping aggregate duration near neutral. Fundamentals are broadly supportive: favor deleveraging corporates, select regional and money-center banks with diversified franchises, and aerospace/defence names; avoid consumer cyclicals and food & beverage credits.

High Yield Credit

High yield debt is cautiously constructive, but geopolitical risk, shifting rate expectations, and structural concerns in private credit warrant selectivity. Spread sensitivity to macro and Middle East shocks means episodic volatility may precede durable recoveries. Favor defensive sectors (utilities, banks, select consumer staples) and resilient subsectors like data centers; avoid discretionary consumer-exposed areas (automotive, leisure, airlines) and vulnerable software issuers. Maintain mostly neutral duration, employ sector tilts, and selectively deploy into well priced primary issuance.

Securitized Debt

Securitized debt enters the quarter cautiously upbeat. Agency mortgage-backed securities (MBS) saw early spread compression, but rising rates and prepayment risks have clawed back some of the gains. Convexity-protected and credit-enhanced mortgage slices look attractive. Asset-backed securities (ABS) fundamentals are mixed, with high income consumers supporting some pools, while subprime auto delinquencies remain elevated. CMBS shows recovery potential in SASB and sponsor-backed deals despite office delinquencies. Collateralized loan obligations (CLOs) face headwinds from private credit underwriting and collateral shocks. Favor front-end to five-year duration, high-quality credit selection, infrastructure-linked ABS, and active, disciplined underwriting.

Private Credit

Private credit faces an inflection point: strong deal flow, durable borrower fundamentals, and rising institutional demand counterbalanced by looser underwriting, liquidity mismatches, and scrutiny, especially among BDCs and broadly syndicated loans where weaker covenants and higher leverage prevail. Discipline favors lower- and core middle-market direct lenders with rigorous underwriting, strong covenants, prudent leverage, and investor alignment. We believe that investors should prioritize managers with conservative structures and alignment to capture attractive risk-adjusted yields as capital reallocates from errant managers into resilient, well-managed segments.

Platform To Digitally Trade Corporate Bonds")