From Daleep Singh, Vice Chair & Chief Global Economist, PGIM, and Guillermo Felices, PHD, Global Investment Strategist, PGIM Credit.

-

The war in Iran has led to a world of thicker tails where the distribution of those risks will largely depend on the length and intensity of the conflict.

-

Despite the disconcerting primary and secondary effects of the war, prominent features of the global economy, including an AI infrastructure boom and the era of fiscal dominance, will continue to influence global outcomes.

We start with our views on the war, which took another turn with the announced ceasefire at the time of publication. If the ceasefire falters, in our adverse scenario—“escalate to de-escalate”—the U.S. administration ratchets up the costs to the Iranian regime through various measures, such as potential strikes on power plants. The operational menu in this scenario is broad, and the constraint is risk tolerance. It thickens the tail risk towards a potential scenario involving a protracted cycle of intensification. This case prompts central banks into growth-stunting rate hikes and dislodged inflation expectations, while economic growth stalls or recedes across economies, and the trading environment unambiguously turns risk off.

In our less-adverse scenario, both sides maintain the fragile “face saving” ceasefire that mostly endures. The hard issues—Iran’s nuclear program, missile arsenal, proxy network as well as the operational oversight of the Strait of Hormuz—are deferred. Both sides claim victory, and the hot war becomes a frozen conflict. Along this path, the Strait mostly reopens, and the U.S. establishes a permanent Gulf presence sufficient for insurance underwriting. Oil prices partially retreat, and rate hikes in oil-consuming countries are generally priced out. Fiscal stimulus cushions growth, particularly in the U.S., while adding to upside inflation pressure. Rate curves remain steeper on overheating risks, which is our modal case for the U.S. economy as we explain below. Risk assets experience an initial relief rally before trading sideways.

The descriptions of our war-related scenarios—the adverse and the less adverse—indicate that there are no “good” options left and that scars from the war will remain for years.

Yet, we see the “less adverse” outcome as more likely based on areas of overlapping interest between the U.S. and Iran, which are grounded in existential political concerns and Iran’s belief that it has re-established deterrence.

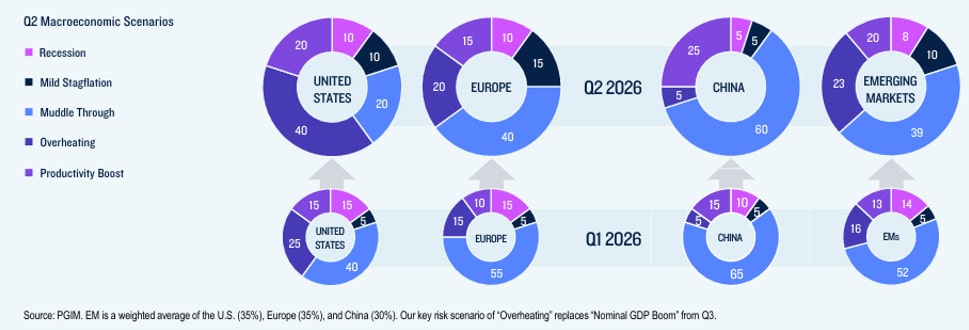

All of which feeds into our “overheating” base case (40% probability) for the U.S. economy over the coming 12 months. This scenario assumes that real GDP growth materially accelerates above trend, driven by AI-related investment, a strong high-end consumer and, crucially, twin stimulus. It also assumes that the weakening labor market and the prospect of a productivity boom will give the Fed leeway to cut policy rates to 3.00-3.25%. At the same time, we expect fiscal policy to remain loose over the forecast horizon. We expect the Iran shock to keep crude oil and other related energy prices elevated for several months, before somewhat normalizing in the second half of the year in line with the Brent oil futures curve (see Exhibit).

Also read: Global Asset Allocation: The View From Australia

Brent Oil Futures Curve (USD per Barrel)

In our view, the energy shock punctures, but doesn’t derail, the strong nominal growth that underpins our base case. It assumes that inflation rises to 3.5% in Q2 before gradually easing towards 3.0% in Q1 2027, while growth eases in Q2 before reaccelerating by the end of the year, potentially aided by further fiscal support related to defense and energy subsidies. In this environment, we think risk assets remain resilient, supported by nominal GDP, but could be checked by the potential un-anchoring of inflation expectations.

Our base case in Europe remains a “muddle through” scenario with a 40% probability as growth increases to about 1.2% year-over-year. We expect a floor under growth due to already committed fiscal support in Germany, Italy, and France. Inflation is expected to peak at around 3.5% in mid-2026 before falling back to 3.0% by year end and then to 2% as the higher level of energy drops out of the year-over-year calculation. The ECB consequently hikes in June and again in September, taking the deposit rate to 2.5%.

Our base case for China is also a “muddle through” scenario with a 60% probability (see the following Exhibit for our emerging market scenario methodology). Under this scenario, China pursues an AI-led industrial policy mix with substantive steps to boost domestic demand. Excess capacity gradually eases, but continues to exert a deflationary impulse globally. Fiscal policy remains accommodative, with calibrated support for the consumer, property sector, and infrastructure.

Q2 Macroeconomic Scenarios

View: Short-term yields remain elevated amid mounting inflation concerns and expectations of more hawkish monetary policies. Long-end yields stay relatively anchored as investors see favorable value at current levels.

The war in Iran and subsequent surge in energy prices quickly flattened developed market yield curves, shaping our expectations looking ahead. Coming into the year, investors spun a comfortable narrative that a gradually slowing global economy caused by a weakening labor market would elicit moderate policy accommodation. The surprise of war and potential inflation boost caused a rapid unwind of these large positions as investors recognized many central banks would be forced to shift from an easing to hiking bias. For example, at the end of February, the market was pricing the ECB to remain on hold, the Fed to cut twice, and the BOE to cut almost three times. Currently, the market is pricing the ECB and BOE to hike twice and the Fed to be on hold for the remainder of the year.

Given the 50-100 bps of front end repricing, most major central banks are indicating a wait-and-see approach as they remain wary of impending inflation as the war continues.

For context, we started the year with an expectation that the U.S. 10-year yield would break out of a prolonged 20 bps trading range on the eventual reemergence of policy uncertainty. While we didn’t anticipate the kinetic conflict in the Middle East, the upturn in volatility materialized late in the first quarter as the 10-year yield approached 4.50% and the 30-year almost touched 5%. We believe yields will find support at the upper bounds of the range.

While the rapid market repricing of the front end may suggest potential Fed rate hikes, we believe recent market moves may be more indicative of the clearing level for risk and changing levels of liquidity as opposed to a wholesale repricing of fundamentals.

Therefore, if the conflict concludes in relatively short order, we see the possibility that rate cuts may still emerge later this year and continue into early 2027. We believe the new Fed Chair could lead the terminal Fed funds rate near 3.0% (see our economics section for more).

Although liquidity across the U.S. rate complex deteriorated as the conflict continued—particularly in front-end futures contracts—the market remained resilient and continued to transfer risk. We believe the majority of the rate shock is behind us and that liquidity will return to more normal levels once conditions in the Middle East stabilize.

")

Platform To Digitally Trade Corporate Bonds")