Monthly Market Views: Fixed income resilience and equity market divergence

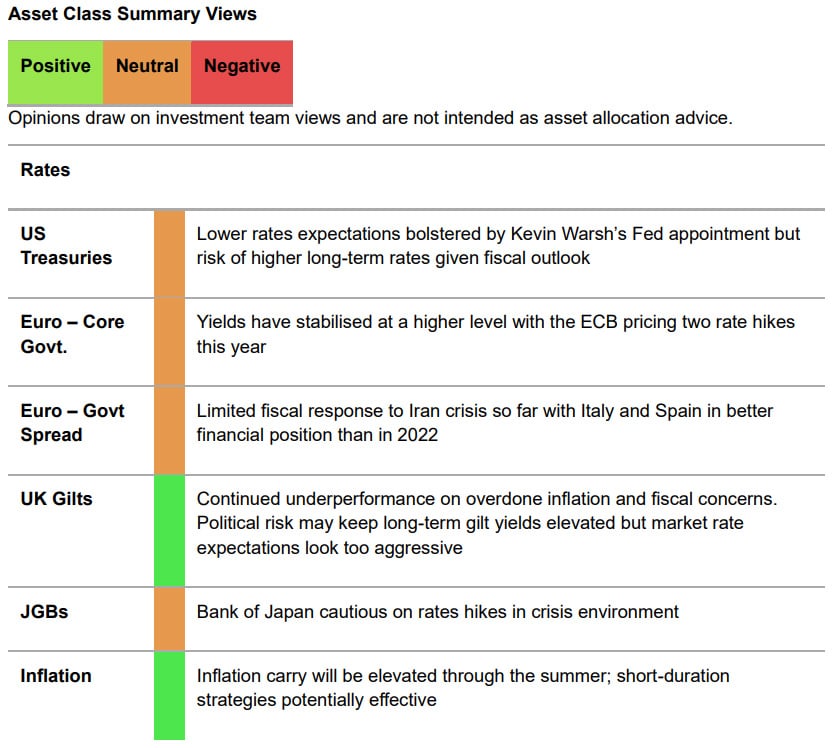

Rate expectations

Fixed income performance has been inversely correlated to duration since the start of the Middle East conflict. The best performers have been those with limited duration, high income levels, or with inflation exposure. US fixed income has tended, in all maturity and credit buckets, to perform best. This is due to US yields being higher than in Europe, and the market expecting a more limited impact on inflation and policy interest rates. If risks around inflation, interest rates, and government finances hold, these trends are likely to persist. Despite rates being left on hold in April, the risk is that they are hiked in the eurozone and UK.

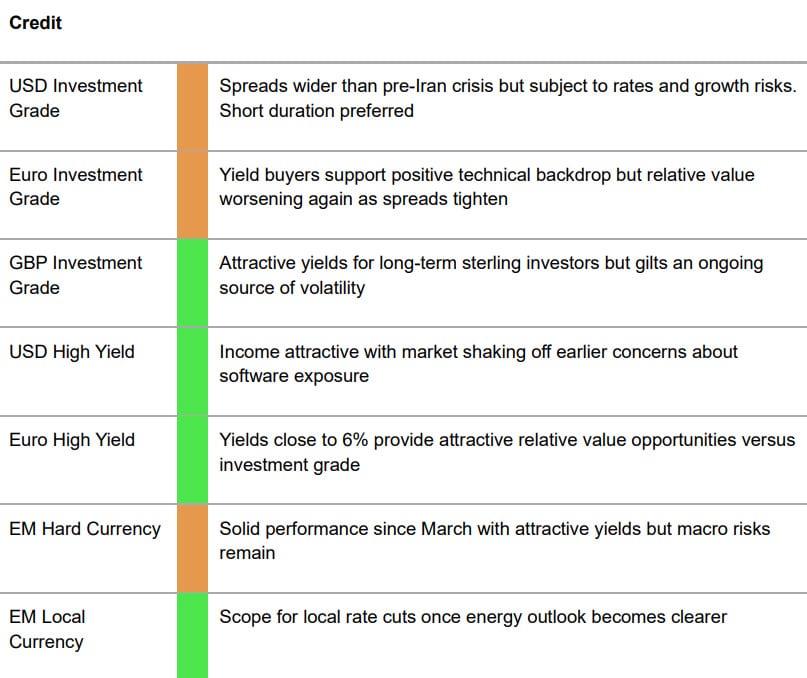

Meanwhile, markets are expecting rates in the US to remain on hold for the rest of the year. For now, US high yield is attractive given its structurally low duration and the significant contribution of income to total returns. From 27 February to 1 May, the income return on the ICE/BofA US High Yield index was 1.2% compared to 0.9% for European high yield and 0.52% for one-to-three-year maturity US Treasury bonds. Better performance from longdated bonds needs an end to the Iran conflict, lower energy prices, and a bullish pivot in rate expectations.

Selective support

The correlation of equity indices with oil prices has partially broken down recently. As of the end of April, Brent oil had rebounded by around 20% over the previous few weeks, while global equities were flat. US returns have been supported by positive economic data and good results from the current earnings season. S&P 500 earnings per share have increased by 20% for the companies that had reported as of the time of writing, with encouraging breadth across sectors. This contrasts with a 7% EPS rise in Europe, which was not enough to prevent the MSCI Europe index from declining. The second divide is between tech and non-tech stocks. For example, within the MSCI Emerging Markets index, the former have significantly outperformed the latter recently.

Looking ahead, once the earnings season is behind us, investors will likely turn their attention back to the Middle East. If oil prices remain high or rise further, we could see another period of weakness in industrial stocks. Sector selectivity will be key. The technology theme, meanwhile, looks to be a sustainable trend.

China’s divergent path to technological innovation

Asian market divergence in the technology sector highlights a dynamic shift in the regional landscape, fuelled by the global artificial intelligence drive. Notably, emerging Asia’s hardware hubs, Taiwan and South Korea, are thriving due to increased demand for high-end semiconductors, largely on the back of the US’s AI capital expenditure. Meanwhile, China is actively working to establish its own technological leadership. Although recent policy reforms and domestic AI innovations like DeepSeek have spurred investment, the sector still trails regional peers in hardware domains, due to ongoing headwinds from US export restrictions.

By some estimates, China’s AI Graphics Processing Units self-sufficiency rate will rise from 41% in 2025 to 76% in 2030.1 As such, China is focusing on improving AI models’ intelligence without significant scaling and/or training with larger datasets. Arguably, for now, China’s AI competitive advantage sits in power, infrastructure, and physical AI. This is not merely coincidental; it reflects China’s strategic pursuit of self-sufficiency. And for investors, China’s idiosyncratic AI story – not a derivative of the US AI theme – implies potential diversification opportunity.

- Source: Morgan Stanley Research, China’s Emerging Frontiers: China’s AI Path: More Bang For The Buck, April 2026.

Platform To Digitally Trade Corporate Bonds")