From Alan Greenstein, Zagga CEO and Co-Founder

For even the most experienced investors, portfolio composition and income generation have become markedly complex. Amidst the hunt for resilience, private credit has earned a reputation as a stabilising force – providing genuine portfolio diversification, stable income, and attractive risk-adjusted returns, when done well.

Yet, as gates close in the US private corporate credit market and the UK and Europe becomes increasingly saturated, many question if the private credit proposition remains compelling.

Australian real estate private credit has largely differentiated itself due to its backing by quality, underlying real assets, a robust and resilient economy, a well-regulated lending market, and the strong tailwinds powering our local property sector.

The world is taking notice. Global capital continues to need a home, and for institutional and sophisticated investors, Australian real estate private credit remains an attractive proposition.

“The global search for stability is on, and Australian real estate private credit may prove a safe harbour from stormy seas elsewhere. Private credit is not a homogenous asset class; we must have our eyes wide open to risk.”

As every facet of financial markets feel the pressure, the focus must be on governance, prudent risk management, and specialised, cycle-tested investment expertise.

The changing investment landscape

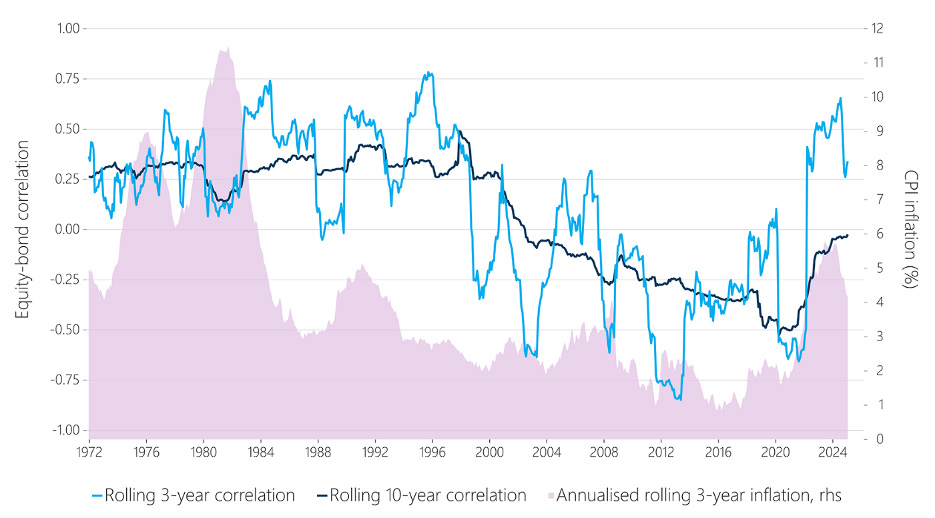

The traditional 60/40 portfolio is under strain, with bonds and equities showing increased correlation, see the chart below.

Investors are turning to alternative asset classes, like private credit, which are unlisted and uncorrelated to the swings of public markets. Private credit returns are typically linked to interest rates, not market sentiment – which can offer stability even amid shifting government policies or macroeconomic uncertainty. Focusing on property-backed private credit adds the structural security of tangible assets, providing a secondary layer of uncorrelated diversification.

In real estate private credit, loans are commonly structured with floating interest rates, meaning returns move in line with the prevailing cash rate, maintaining a consistent margin above the benchmark.

The appeal of this strategy is evident in the growth of private credit. Globally, private credit is a USD $1.96 trillion market, forecast to grow to almost USD $3.5 trillion by 20311.

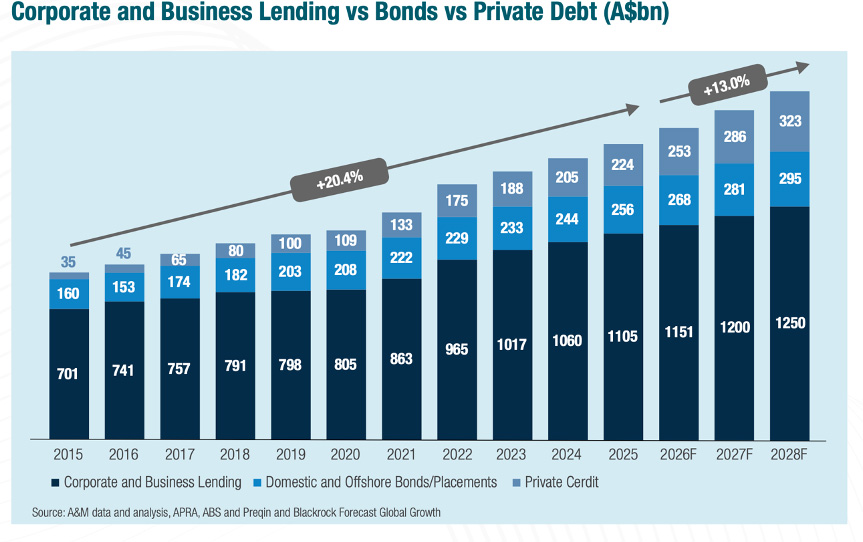

“Asia Pacific is the fastest growing region, globally, for private credit, with 12.5% CAGR2. The Australian market alone is growing by 9% YOY with the local private credit market now valued at AUD $224 billion in assets under management3.

“Commercial real estate lending accounts for ~18% of the Australian private credit market, with AUD $92 billion invested4, and growing.”

A nuanced global story

Despite strong tailwinds, the global private credit market has faced its share of challenges this year, with investors growing wary of liquidity risk, opacity, and manager expertise.

This rhetoric has largely been driven by the US, where current “doom and gloom” narratives focus on market structures, exposures, and legal frameworks that differ meaningfully from those in Australia.

As several leading US fund managers gated redemptions on retail funds this year, the risks of private credit came sharply to the fore. In the US, private credit is concentrated in corporate lending, often involving leveraged borrowers and complex capital structures. It is also heavily exposed to the technology sector, which is facing significant disruption and declining valuations due to AI. While this segment of the US market offers attractive yields, it is increasingly facing scrutiny over widespread, systemic risks. Too much capital is chasing too few high-quality deals, default risks are rising, underwriting standards have loosened, and the ecosystem is expanding faster than its underlying fundamentals and risk controls5.

On the other hand, the UK and Europe have been criticised for being stagnant. The market is saturated and capital is struggling to find a home. With persistent economic uncertainty, and geopolitical turmoil on their doorstep, growth has slowed to a trickle. Competition has become unhealthy, leading to margin compression, tighter spreads, lower yields, and less attractive risk-adjusted returns.

This global dynamic has highlighted that not every private credit investment can be examined through the same risk lens. For example, the risk profile of US corporate credit is fundamentally different from real estate private credit in Australia, which is secured and underpinned by physical assets.

Uncertainty sharpens the focus on fundamentals. It forces investors to ask better questions – not just about returns, but about risk, structure, and governance. Because beneath a single label sits a wide spectrum of investment opportunities and varying degrees of risk. In today’s environment, understanding those distinctions is critical.

Local stability attracts international attention

A changing global landscape has driven institutional and sophisticated investors to hunt further afield for diversified, defensive investment opportunities. As global capital searches for a home, Australia may prove itself as the place to be. Renowned for its stable regulatory environment, transparent legal system, resilient, demand-driven economy, and sophisticated financial services and pension sector, Australia has established itself as an investment destination of choice.

The stability of our market is evident when compared with our global peers, including the US, UK, and Europe. We have strong credit controls, a AAA rating on sovereign debt, a tight labour market, and a resilient underlying economy. We also have significantly more room for private credit growth when compared with mature markets, like the US and UK, at a time when traditional lenders are pulling back due to capital and regulatory constraints.

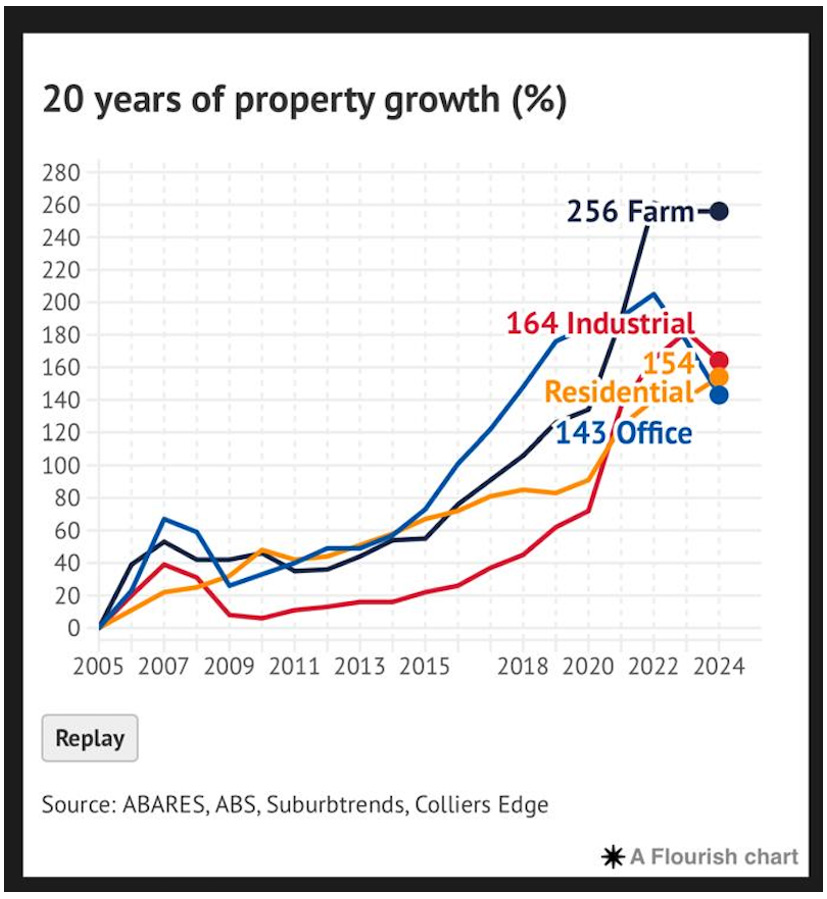

These fundamentals are underpinned by a robust and expanding property market. Fuelled by 20 years of sustained growth, the structural imbalances in Australian real estate present a compelling opportunity. Australia has one of the fastest growing populations in the western world, driven by strong immigration, and currently faces a shortage of ~262,000 dwellings6. The government had set a target of 1.2 million new homes by 2029, delivering industry reforms and favourable policy designed to drive housing growth.

Further strengthening the investment case are recent Australian Securities and Investments Commission (ASIC) regulatory reforms, designed to establish minimum standards and operating protocols in Australia’s private credit sector.

Capital follows opportunity

Australia’s economic strength, especially compared with global peers, has attracted substantial international capital into private credit, including from insurance funds, family offices, and high-net-worth investors7.

“Global capital is recognising the favourable conditions in Australian real estate private credit and inflows are surging.”

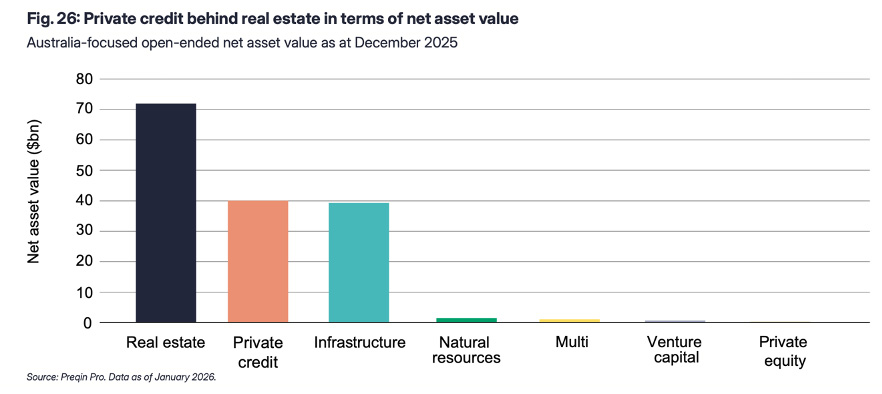

Real estate and private credit are now the largest sources of open-ended funds by net asset value in Australia, with the number of private credit funds tripling since 20178 and increased allocations from global investors anticipated in the near term.

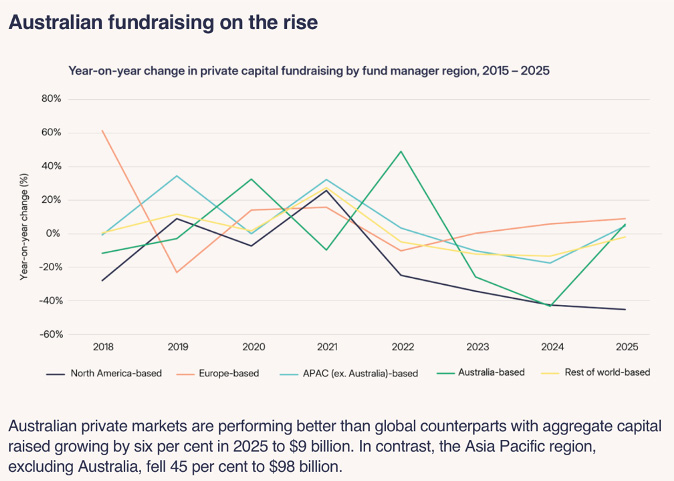

More broadly, fundraising in private markets is on the rise with Australia outperforming its global counterparts, including the Asia Pacific region.

This is not an isolated, short-term trend. Private credit in Australia has been growing consistently for more than a decade, moving from a niche option to a significant, rising source of commercial financing. It has now outpaced traditional bank debt and bond markets, with a compound annual growth rate (CAGR) of 21% over the last decade9, compared with ~5% for banks and bonds10.

Furthermore, UBS data highlights almost 80% of family offices intend to maintain or grow their private credit allocations over the next five years11.

There is significant potential for well-credentialed Australian private credit managers to attract more offshore capital, particularly from the ASEAN region, with sophisticated investors attracted by the diversification and defensive qualities Australia’s economy has to offer.

Time for experience and discipline

The increasing flow of offshore capital into Australian private credit highlights the market’s growing scale but also elevates the need for deployment discipline and specialist expertise. Despite ongoing expansion in Australian real estate private credit, current macroeconomic headwinds require investors to maintain a highly selective approach when assessing opportunities.

As macro conditions intensify, both locally and globally, the expertise and execution of real estate private credit managers will be tested. With headwinds on the horizon, managers must strengthen project due diligence and ensure feasibility and sustainability in an environment defined by uncertainty.

Now is the time for experience and discipline. For investors, manager selection is crucial and cycle-tested managers with specialist expertise, robust governance frameworks, and transparent investment practices will have a clear advantage.

“An experienced manager with a proven track record, which understands recovery processes, maintains strong counterparty relationships, and can act decisively to protect investor capital. This is where experience and discipline can translate directly into returns.”

As investors fortify portfolios, we must remember that private credit investments do not all share the same attributes and cannot be uniformly assessed. Proactive due diligence to understand the underlying investment and associated risks will help investors seize the right opportunity and move portfolios from risk to resilience.

A cautiously optimistic outlook

As private credit moves from an alternative asset to a core part of a well-balanced portfolio, the long-term outlook remains positive for our sector. Australia’s economic fundamentals remain strong, our housing supply imbalance provides significant tailwinds, and, as such, our market continues to attract new capital and attention from both domestic and offshore sophisticated investors. This is playing a critical role in establishing a more mature private credit market with better structures, stronger governance, and greater scrutiny.

Yet, with macro uncertainty rife, investors would be wise to focus on the fundamentals by prioritising governance, prudent risk management, and specialised, cycle-tested investment expertise over headline returns that may carry outsized risk. Incorporating uncorrelated asset classes into portfolios can be a way for investors to diversify against the fluctuations of public markets to manage overall risk-return dynamics within a broader portfolio.

As investors hunt for opportunity through uncertainty, Australian real estate private credit remains an attractive proposition. Global capital needs a home and Australia remains a worthy contender.

[1] https://www.mordorintelligence.com/industry-reports/private-credit-market

[2] https://www.actuarialpost.co.uk/downloads/cat_1/Aon-2026-cat-recap.pdf

[3] Alvarez & Marsal, Australian Private Debt Market Review, November 2025

[4] Alvarez & Marsal, Australian Private Debt Market Review, November 2025

[5] https://www.fsb.org/2026/05/fsb-warns-on-private-credit-vulnerabilities | https://www.forbes.com/sites/mayrarodriguezvalladares/2026/05/24/rising-private-credit-defaults-are-testing-banks-and-insurers | https://www.reuters.com/sustainability/boards-policy-regulation/watchdog-flags-risks-banks-growing-private-credit-ties-2026-05-06

[6] National Housing Supply and Affordability Council, May 2025

[7] Australian Investment Council, Australian Private Capital Yearbook 2026

[8] EY-Parthenon Annual Australian Private Debt Market Overview, March 2026

[9] EY-Parthenon Annual Australian Private Debt Market Overview, March 2026

[10] Alvarez & Marsal, Australian Private Debt Market Review, November 2025

[11] UBS Global Family Office Report, 2025

Zagga is an Australian fund manager specialising in real estate private credit through both managed funds and direct investments. With solutions across the capital stack, it specialises in mid-market loans, ranging from AUD $10M to $150M. Since originating its first loan in 2017, Zagga has funded over AUD $3 billion in real estate transactions, completed more than 350 successful exits, and repaid over AUD $1.5 billion in principal and interest to its investors.

")

Platform To Digitally Trade Corporate Bonds")