Thomas Poullaouec, Head of Global Investment Solutions, International and Portfolio Manager at T. Rowe Price, and his team have published their latest insights on global asset allocation and the investment environment for Australia. June 2026.

OUTLOOK

Despite heightened geopolitical tensions that continue to fuel inflation pressures and weigh on growth, markets have remained remarkably resilient, supported by fiscal spending and ongoing investment, particularly in AI infrastructure.

In Australia, rising inflationary pressures raises the risk of the economy falling into stagflation, complicating the outlook for domestic equities and rates.

The monetary policy outlook has become increasingly complex as central banks balance persistent inflation pressures stemming from geopolitical conflict against signs of slowing economic activity and a soft labor market.

Key risks include a further escalation of the conflict with Iran, a sustained rise in energy prices, greater reliance on a narrow set of growth drivers, and signs of deterioration in labor markets and private market liquidity

THEMES DRIVING POSITIONING

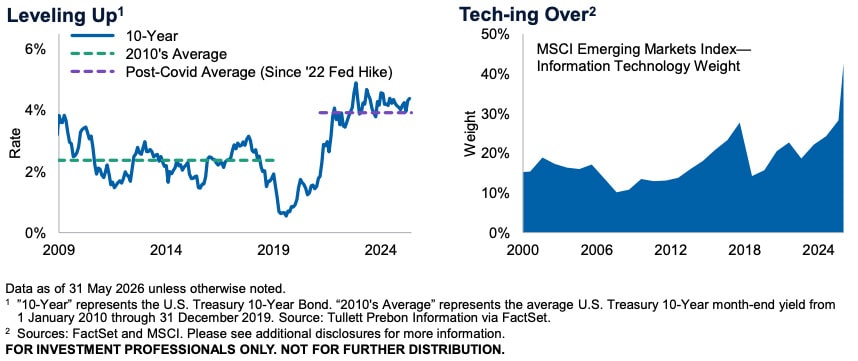

Higher-for-Ever

The Iran war and resulting energy shock have pushed oil prices higher, adding to input costs, headline inflation, and inflation expectations. As a result, global interest rates have moved higher and central banks, including the Federal Reserve, have become more cautious about easing policy. More concerning, however, is that even if the current energy shock eventually fades, several structural forces suggest that the floor for interest rates could remain higher than it was over the previous decade. The global economy is requiring greater investment, with spending needs rising across AI infrastructure, defense, energy security, and grid resilience. At the same time, persistent fiscal deficits and elevated debt issuance are likely to keep pressure on government bond markets. Longer-term yields also appear to reflect a higher term premium, as investors demand greater compensation for inflation volatility, fiscal uncertainty, and geopolitical risk. Taken together, these forces suggest that interest rates may remain structurally higher than many investors expect, supporting our shorter-duration stance.

Also read: A New Era For The Fed

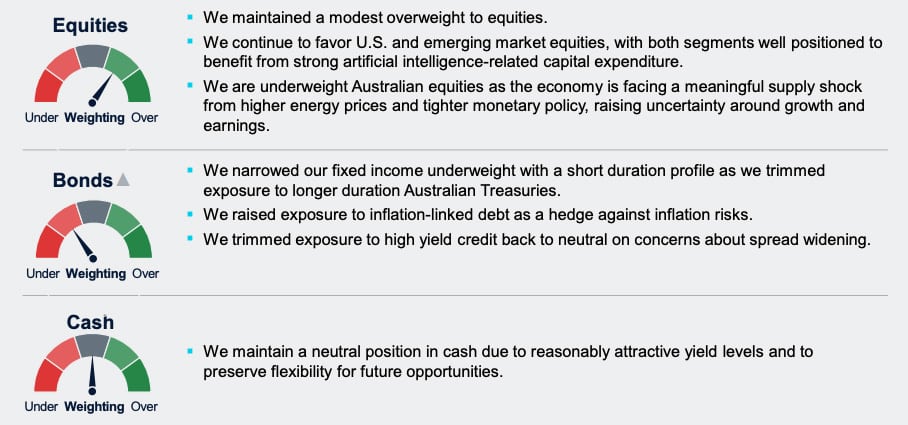

From Commodities to Code

The MSCI Emerging Markets Index has changed meaningfully, with technology rising from 24% of the benchmark at the end of 2024 to roughly 42% today, shifting the nature of emerging market (EM) equity exposure. Investors may still view EM as a play on regional economic growth, commodities, Chinese consumer demand, and global trade, but the asset class is increasingly tied to AI infrastructure, semiconductors and digital platforms. This does not mean EM has become less cyclical; rather, the source of cyclicality has shifted. EM may now be more exposed to semiconductor cycles, hyperscaler capex, AI sentiment, and broader investor appetite for growth stocks. For cross-asset investors, EM allocations may be taking on more technology and growth exposure than many realize, bringing underappreciated concentration and correlation risks. However, this shift also improves EM’s exposure to structural earnings growth, supporting our overweight to EM equities.

ASSET CLASS POSITIONING

Note: T. Rowe Price’s Australia Investment Committee comprises local and global investment professionals who apply views from the firm’s Global Asset Allocation Committee to make informed asset allocation views from an Australian investor perspective. The Committee is led by Thomas Poullaouec, Head of Multi-Asset Solutions APAC, based in Singapore.

")

Platform To Digitally Trade Corporate Bonds")