At its June meeting, Kevin Warsh’s first as chair, the Federal Open Market Committee (FOMC) left the target range for the federal funds rate unchanged at 3.50%-3.75% for a third consecutive meeting.

The meeting marked a clear shift in communication, framing, and policy process, even if the policy decision itself was uneventful. There were 5 key takeaways:

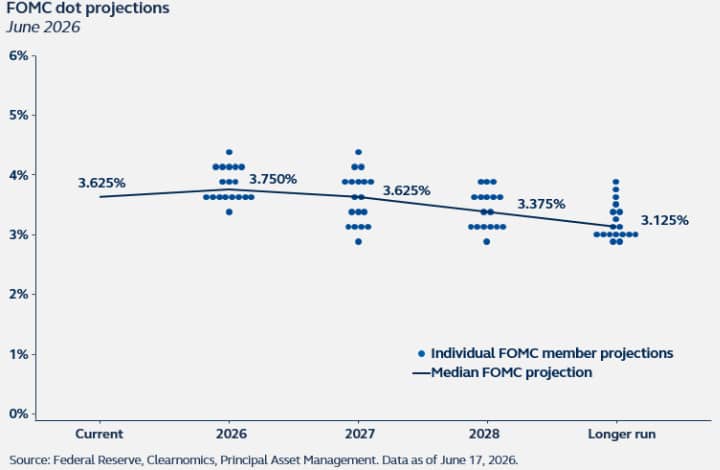

1. The dot plot turned more hawkish, with 9 of 18 participants expecting at least one hike this year.

2. Chair Warsh did not submit a dot, reinforcing uncertainty around his policy bias.

3. Forward guidance has effectively been abandoned, with a clear move away from pre-committing on rates.

4. There was greater emphasis on price stability, with limited explicit reference to the dual mandate.

5. A structural reset is underway. Five task forces were launched to review communications, the balance sheet, data and measurement, productivity/jobs, and the inflation framework.

A different Fed

The meeting marked a clear break from the Powell-era communication style. Warsh offered little incremental guidance, repeatedly referring to the formal statement, which described an economy expanding at a solid pace, supported by strong productivity and capex, with unemployment stable and inflation elevated.

Additional color was limited. The key nuance was that policy appears restrictive for housing, but less so for the broader economy. Beyond this, the emphasis was on signaling a shift in approach—away from forward guidance and toward a broader reassessment of policy and communication. In several instances, questions were effectively deferred on the basis that “there is a task force for that.”

Also Read: Fed Policy Direction Under New Chair

In practice, the absence of forward guidance has shifted market focus onto the Summary of Economic Projections (SEP) and the dot plot—the very tools Warsh appears least inclined to rely on. As a result, the meeting has been interpreted as relatively hawkish, driven largely by the distribution of rate expectations.

Summary of Economic Projections

The June SEP showed meaningful changes across economic forecasts and the median policy path.

· Growth: GDP growth was revised down from 2.4% to 2.2% for 2026, but was unchanged at 2.3% for 2027, and revised up from 2.1% to 2.2% in 2028. The longer‑run growth rate was unchanged at 2.0%.

· Labor market: The unemployment rate forecast was nudged down from 4.4% to 4.3% for 2026 but left unchanged for 2027 and 2028 (4.3% and 4.2% respectively).

· Inflation: Headline PCE inflation for 2026 was revised up from 2.7% to 3.6%, and from 2.2% to 2.3% for 2027. Core PCE was also raised from 2.7% to 3.3% for 2026, and from 2.2% to 2.5% in 2027, with the 2% inflation target not reached until 2028.

· The median dot: 9 of the 18 dots showed tightening in 2026, with 3 members projecting one 25 bps hike, and 6 projecting 50 bps of hikes. Importantly, one dot was missing—Fed Chair Warsh’s. Note that the median dot shows the fed funds rate at its current level in 2027 and 25 bps lower in 2028.

NextGen Fed chair

Warsh appears to be ushering in a more introspective Fed, willing to revisit core elements of the framework. While reviews of communications and the balance sheet were expected, the inclusion of data quality, productivity dynamics, and labor market measurement marks a more ambitious agenda.

This reflects increasing concern around the reliability of traditional data. Labor market indicators, for example, rely on surveys with declining response rates and are subject to significant revisions. At the same time, structural forces—particularly technological change—are complicating the relationship between growth, employment, and inflation.

Against this backdrop, the decision to deepen analysis in these areas is timely. The review of the inflation framework is also likely to focus on which drivers of inflation monetary policy should respond to, particularly in a more geopolitically volatile environment. Importantly, Warsh reaffirmed commitment to the 2% inflation target, signaling evolution rather than a change in objective.

Policy outlook

Markets have responded by pricing a more hawkish path, with front-end yields rising sharply, equities softening, and the U.S. dollar strengthening. Investors now discount roughly 50 bps of tightening by early 2027.

In our view, this may overstate the near-term policy impulse. The bar for further tightening remains high and would likely require sustained economic strength, renewed firmness in core inflation, and signs that inflation expectations are becoming less well-anchored. While inflation forecasts have moved higher, forward-looking risks may be more balanced.

Indeed, even Warsh noted that committee expectations reflect a level of uncertainty and will likely be dependent on how economic and geopolitical conditions evolve from here. Tentative progress towards a U.S.-Iran agreement, for example, suggests that energy-related inflation pressures could peak sooner and at a lower level than previously feared.

Against this backdrop, while a hike remains more likely than an easing, the most plausible path is continued policy stability in the near-term. With uncertainty elevated and the Fed engaged in a broad internal review, holding rates steady through year-end remains the base case.

")

Platform To Digitally Trade Corporate Bonds")