Thomas Poullaouec, Head of Multi-Asset Solutions APAC at T. Rowe Price, and his team have published their latest insights on global asset allocation and the investment environment for Australia. February 2026.

OUTLOOK

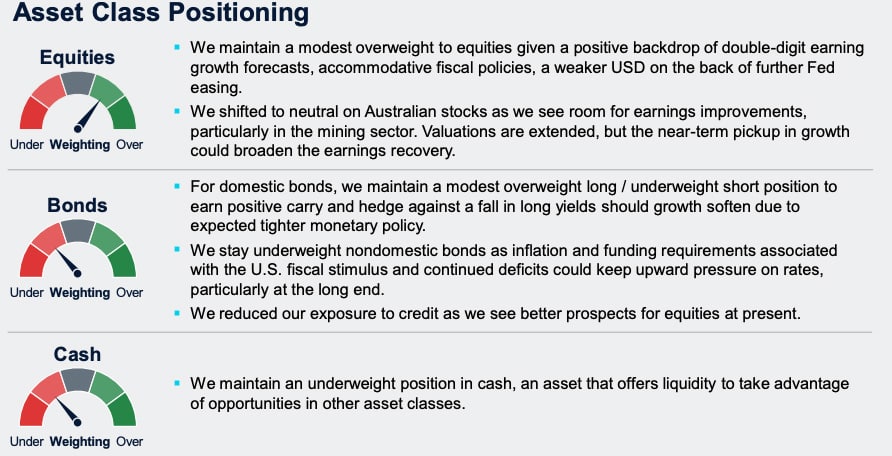

We maintain a relatively balanced view across global risk assets with a modest overweight in equities. Despite extended valuations, earnings trends and economic growth remain favorable.

U.S. economic growth remains resilient, fueled by AI-driven capital spending and supportive fiscal and monetary policies, although labor market data continues to reflect a softening.

In Australia, sticky inflation reinforces the central bank’s “higher for longer” stance, but improving private sector activity, sustained capital spending globally and Chinese stimulus should be near-term tailwinds for the economy.

Markets outside the U.S. continue to benefit from improving fundamentals, supported by fiscal spending, notably in Europe and Japan.

Key risks to global markets include any threat to AI-driven growth, sticky inflation, a sharper-than-expected deterioration in labor markets, shifting policy expectations, and persistent geopolitical tensions.

THEMES DRIVING POSITIONING

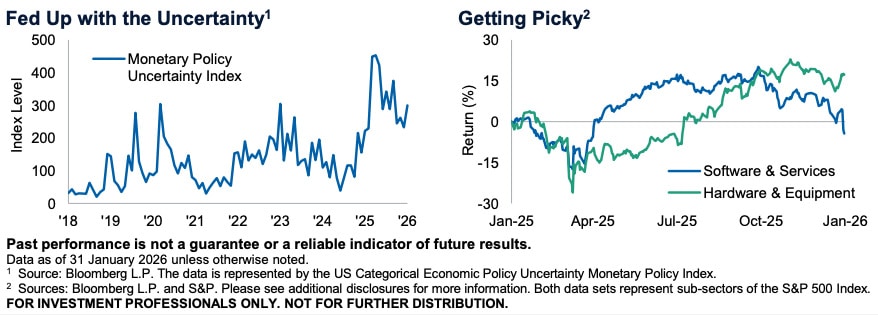

A surprising Fed Nomination

The nomination of Kevin Warsh as Federal Reserve chair has introduced fresh uncertainty into an already delicate monetary policy backdrop. Markets initially recoiled on the news, seeing Warsh as more hawkish given his past criticism of quantitative easing adopted after the Global Financial Crisis. Given the ongoing pressure from the administration to lower rates, Warsh seemed like the most hawkish among the potential candidates. And while he may have had hawkish views in the past, his recent comments on deflationary impacts of AI-related productivity and tariffs being a one-time hit to inflation suggest a more dovish view. Those softening inflation views could be challenged as fiscal policy tailwinds begin to hit what appears to be an already resilient economy. With this clouded backdrop and more division expected among the Federal Open Market Committee, we think the new Fed chair may surprise the market.

Also read: Global Credit Markets and Spreads

Resistance

Despite still broadly positive AI-related news, market sentiment has turned more cautious. Large scale capex commitments to fund AI growth, that had been cheered last year, are now being met with greater skepticism as investors question the return on investment. While the AI theme has broadened to support other parts of the market, other sectors

that might be disrupted by AI have found themselves in the crosshairs, notably software companies. The sector has been hit by fears that AI technology could displace software

services and data analytics firms, with companies potentially developing their own in-house solutions using AI. The combined concerns over AI spending and potential disruption have pressured the technology sector, leaving it trailing most sectors of the market. As valuations continue to reset, we’d expect investors to reengage given the still powerful growth potential for AI. But perhaps we’ve met a healthy point of resistance where investors are becoming more selective in distinguishing potential winners and losers.

ASSET CLASS POSITIONING

Note: T. Rowe Price’s Australia Investment Committee comprises local and global investment professionals who apply views from the firm’s Global Asset Allocation Committee to make informed asset allocation views from an Australian investor perspective. The Committee is led by Thomas Poullaouec, Head of Multi-Asset Solutions APAC, based in Singapore.

")

Platform To Digitally Trade Corporate Bonds")