Thomas Poullaouec, Head of Global Investment Solutions, International and Portfolio Manager at T. Rowe Price, and his team have published their latest insights on global asset allocation and the investment environment for Australia. April 2026.

OUTLOOK

Continued conflict in the Middle East and energy supply shock threaten higher inflation and weaker growth, particularly in energy-import dependent economies.

Regional sensitivity to the energy crisis is differentiated, with Europe, Japan, and emerging markets more vulnerable due to their dependence on oil and gas imports, whereas the U.S. is self-sufficient in terms of energy supply.

Australia is also exposed to global energy shocks that could add to upside inflation risks, but healthy credit growth, commodity tailwinds, and positive earnings inflections in the financial and materials sectors should support the market.

Key risks to global markets include escalating geopolitical tensions, a resurgence in inflation, reliance on AI-driven growth, further deterioration in labor markets, and a widening of liquidity concerns within private credit.

THEMES DRIVING POSITIONING

War Premium

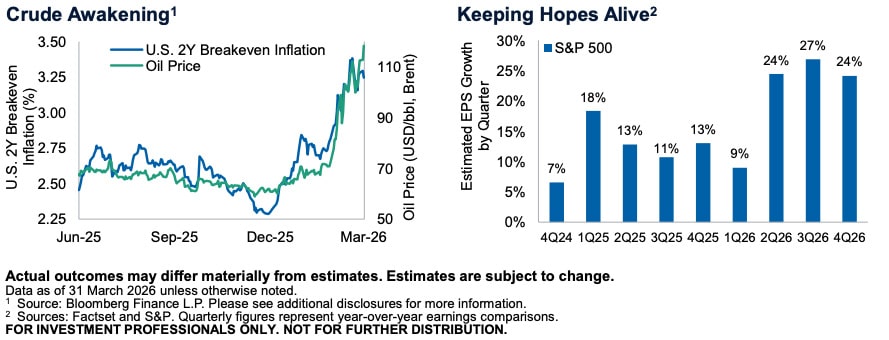

While the recent truce has temporarily brought relief to energy prices, the conflict in Iran remains unresolved with the parties still far apart on demands, raising concerns of continued uncertainty with further escalation not off the table. While energy importing countries remain the most vulnerable, the U.S. is not immune to the impacts, despite its energy independence. Higher global energy prices still filter into domestic costs, from fuel to transportation and beyond. And while the energy impacts could be fleeting with a durable end to the conflict, there are longer-term costs to be paid as seen in the recently proposed nearly 50% year-over-year increase of the 2027 U.S. defense budget ask, with a large portion to fund the conflict in Iran. This comes on the back of increased fiscal spending related to the One Big Beautiful Bill, estimated to add nearly 4 trillion USD in debt, which had already raised concerns over U.S. spending and inflation. While the timetable remains uncertain with the conflict, the combination of energy supply constraints and higher debt levels is bringing inflation concerns back to the forefront, having us lean into inflation hedges.

Also read: Private Credit Headwinds Move Onshore

The Stalwart

In the face of heightened geopolitical tensions in the Middle East, it has been surprising to see the relative resilience of most equity markets across the globe. Some suggest it reflects an optimistic view that the U.S.-Israel war with Iran will be short-lived. But as the conflict drags on and the stakes rise, it is becoming a more uncertain bet. Where we are finding more certainty is in earnings resilience, continuing to prove a stalwart amid heightened geopolitical risk over recent years, with this year’s earnings expectations accelerating from already strong levels supported by fiscal spending, capex, tax incentives and AI-related broadening. Now with the earnings season about to kick off, investors will be eager to hear if the current risks are beginning to weigh on outlooks. But at least for now, earnings momentum seems to be helping underpin the market and supporting our view that broadening can continue, provided the conflict does not materially worsen.

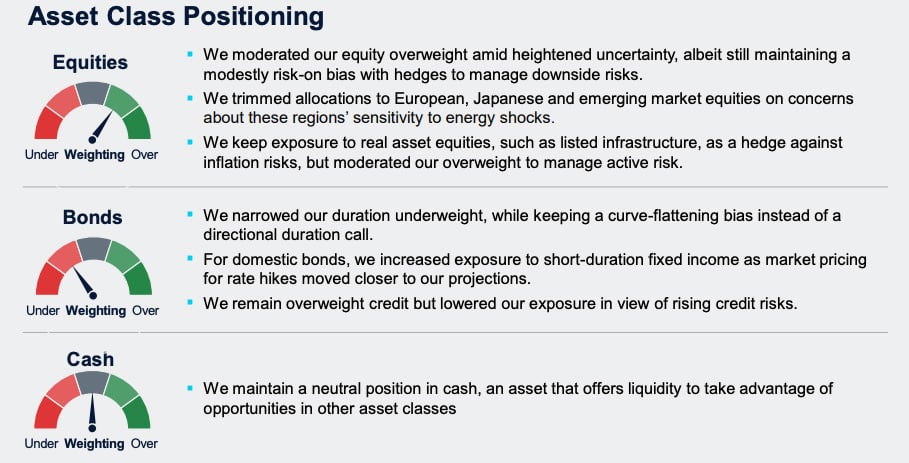

ASSET CLASS POSITIONING

Note: T. Rowe Price’s Australia Investment Committee comprises local and global investment professionals who apply views from the firm’s Global Asset Allocation Committee to make informed asset allocation views from an Australian investor perspective. The Committee is led by Thomas Poullaouec, Head of Multi-Asset Solutions APAC, based in Singapore.

")

Platform To Digitally Trade Corporate Bonds")

Trust")