Amid the resurgence of market volatility from US President Trump’s tariff threats, broader policy uncertainty, and elevated equity market valuations, there is a worthy discussion to be had on whether certain asset classes are providing investors sufficient return relative to their evolving risk profiles. Of course, the asset class in the spotlight is bank stocks.

So looking at bank-issued securities, what are the main income options available to retail investors and how do they stack up in today’s market? Options range from term deposits at the top, all the way down to stocks at the bottom (of the capital stack). The core focus however will be the middle of the capital stack, namely bank debt. Current circumstances are such that bank issued debt securities are offering superior income returns to bank stocks (dividends), and with materially less risk of capital loss.

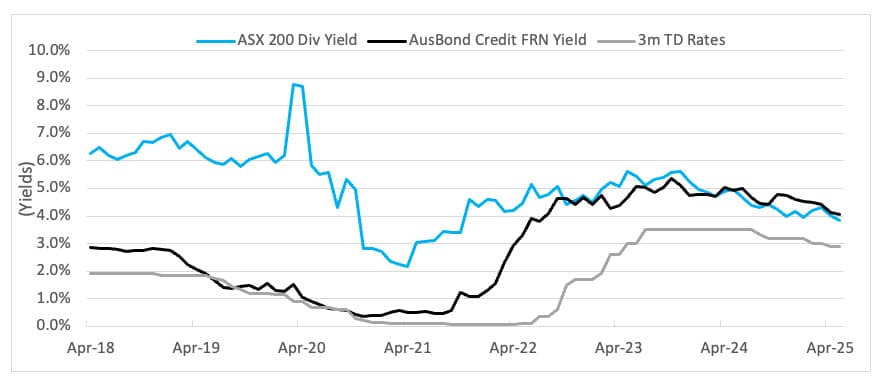

Term Deposits or TD’s offer investors a modest relative income return with no capital downside, and no capital upside. Retail TD rates are anywhere between 2.90% for 3-months up to 3.90% for 12—months per RBA statistics. Not that exciting, but safe.

At the other end of the risk-return spectrum is bank stocks. Over the long-term bank stocks, have delivered decent returns, both in income generation (dividends) and capital gains (share price). Since the turn of the century, the ASX 200 Bank Index has returned a cumulative annual growth rate of +3.3% per annum, while the average annual dividend yield has been around 5.5% per annum. The prevailing dividend yield is 3.8%, well below historical averages.

Despite bank stock prices increasing over the long-term they are susceptible to episodes volatility. Take the past year for example, the ASX 200 Bank Index experienced six separate episodes where the index fell anywhere between 7.5% and 10.3% over the space of 1 – 2 weeks.

Other examples of considerable systemic stress include the GFC in 2008, when the index lost 45% and COVID in 2020 when it lost 36%. Over these two periods bank dividends – per the index – fell 20% and 64% respectively, a meaningful loss of income for those who rely on it for their day to day living.

Also read: Iran Conflict Sparks Geopolitical Shockwave as Markets Brace for Impact

An alternative to bank stocks for income comes in the form of bank issued floating rate notes. These notes are a core component of bank’s ongoing wholesale funding needs, issuing circa $25bn to $30bn per annum, across both senior and subordinated floating rate notes. An index of bank floating rate notes (Bloomberg AusBond Credit Floating) saw falls of just 1.8% and 1.0% respectively through the GFC and COVID.

Floating rate notes are traded (over the counter, not exchange) debt securities that pay coupons every 90-days. They’re also known as credit securities. Coupons are determined based on a margin over the 90-Day Bank Bill Swap Rate and reset every 90-days. Common maturities for floating rate notes are three or five years. Because floating rate notes are debt securities, they represent contractual obligations of the bank and as such must be paid before dividends can be paid. Dividends on the other hand are discretionary – i.e. payment is not guaranteed.

As things stand, and have done so for a year or two now, bank floating rate notes offer a superior risk adjusted return for retail investors. The ASX 200 Bank index dividend yield is 3.8% compared to the yield on the Bloomberg AusBond Credit Index is yielding around 4.1%. Importantly, this index only includes senior ranked bank floating rate notes. If we add in subordinated notes, the yield increases to around 5.3%. So, floating rate notes offer better yield (charted below), but also materially less capital downside during such uncertain times. The return volatility of the ASX 200 Bank index is 28x greater than the return volatility on the Bloomberg AusBond Credit Index.

An asset class that we’ve ignored in the bank capital stack so far in this discussion is hybrids, or AT1 capital. The banking regulator, APRA, declared late last year that AT1 capital was no longer fit for purpose and as such was to be phased out and replaced by tier 2 debt, also known as subordinated debt. Existing hybrids have held up well, attracting a scarcity bid, with the last At1 security to be completely phased out by 2032. During the aforementioned periods of heightened volatility, hybrids saw losses around 20%.

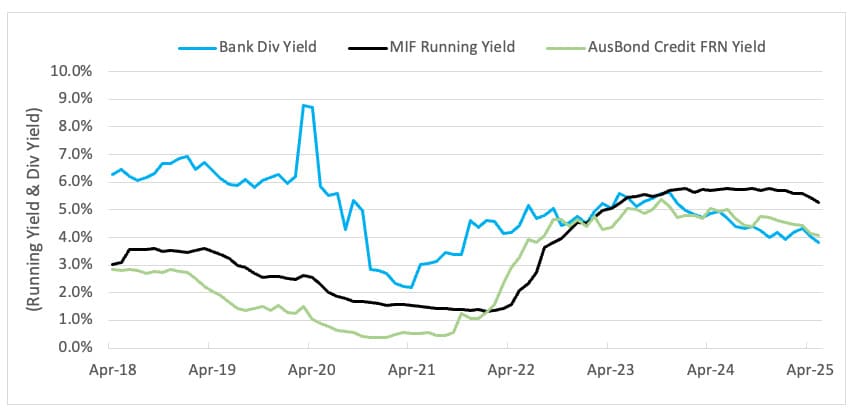

Bank-issued floating rate notes are typically only available to wholesale investors. As a result, retail investors seeking access to this asset class generally need to do so via managed funds that specialise in credit securities, including senior and subordinated bank debt. These funds currently offer yields in the range of 5.0% to 5.3%, depending on their composition and credit exposure.

")

Platform To Digitally Trade Corporate Bonds")