Australia’s 2026 Budget reshapes investing: proposed CGT and negative gearing changes make income assets more attractive, says Income Asset Management’s Jon Lechte.

More Powerful Than Ever: The Era of Income Has Arrived

The 12 May Budget proposes sweeping changes to CGT, negative gearing and discretionary trusts, but leaves coupon income untouched. If legislated, it would be the most significant structural tilt favouring income yield over capital gains in a generation.

If The Tax System Rewrites The Rules, Income Investors Are Already Holding A Winning Hand

The widespread backlash against the 2026 Federal Budget has been well documented. Much of the concern centres on the compounding effect of the proposed CGT framework on diversified portfolios: under indexation, losses on underperforming holdings do not index up to offset gains on the winners. The more diversified the portfolio, the worse the outcome could be.

For retirees in particular, a proposed 30% CGT minimum floor would be highly punitive relative to the marginal rate on the first $45,000 of income, which can sit below 10%. If the measures pass, this would create a structural incentive to reconsider the allocation of capital out of investment properties and other high capital-growth assets, which Australian investors have historically held in excess relative to global peers, and into income-producing assets.

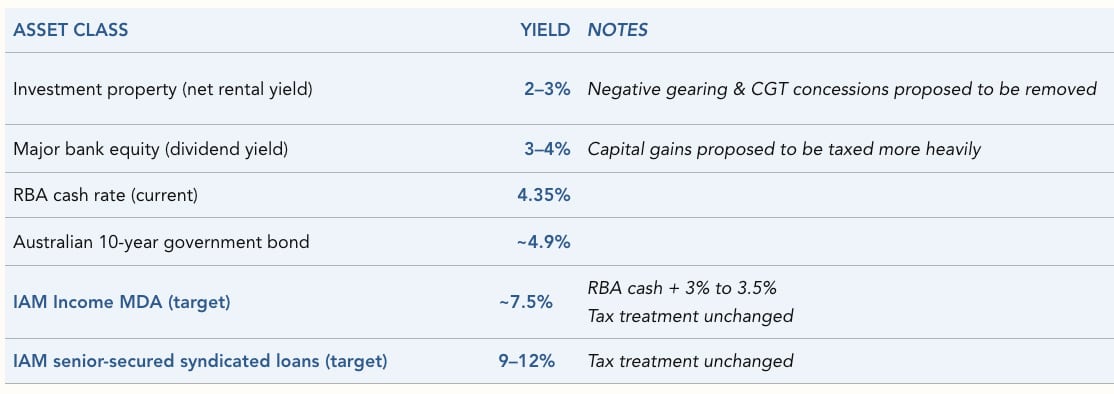

The comparison, even on proposed figures, is stark. A 6.25%+ major bank Tier 2 bond now looks compelling against a 2–3% net rental yield that could lose both negative gearing and CGT concessions, or a bank equity dividend yield of 3–4% where any capital appreciation would be taxed more heavily.

The goalpost has shifted in favour of income solutions: the tax treatment of coupon income has not changed and is not proposed to change.

IAM manages the Income MDA, targeting the RBA cash rate plus 3–3.5%, which equates to roughly 7.5% in today’s environment. At 7.5% reinvested, $1 million becomes $2.06 million in a decade, with no market re-rating required. That is the compounding power of income in an environment where its tax treatment has not changed, and the tax treatment of capital gains may be about to.

Illustrative Yield Comparison

")

Platform To Digitally Trade Corporate Bonds")