A real fear, now largely passed

When the United States and Israel struck Iran on 28 February 2026, the most immediate market concern was an energy-driven inflation shock. That concern was well founded. With the Strait of Hormuz effectively closed to tanker traffic, West Texas Intermediate (WTI) crude rose from around US$67 a barrel on the eve of the strikes to a peak near US$119 in early March, a gain of roughly 78 per cent. A sustained move of that magnitude would have fed directly into headline inflation, hardened central bank policy and pressured bond markets. The fear was real and, at the time, entirely rational.

Almost four months on, the commodity at the centre of that fear has largely retraced its move. Following the framework agreement between Washington and Tehran to reopen the Strait, WTI has fallen back to about US$76 a barrel. It is now only modestly above its pre-war level, around 13 per cent higher than the 27 February close, and the runaway oil price that markets feared has not materialised. Oil remains slightly elevated, but the inflation transmission belt it represented has, for now, been switched off.

Equities have decoupled

Equities have done more than recover. After an initial drawdown of close to 9 per cent into late March, the S&P 500 has taken on a life of its own, pushing through its pre-war highs to record levels around 9 to 10 per cent above where it sat before the strikes. The equity market is no longer trading the war; it is trading resilient corporate earnings, the continued build-out of artificial intelligence and the supportive effect of loose fiscal policy. Whatever the oil price did, equity investors have chosen to look through it.

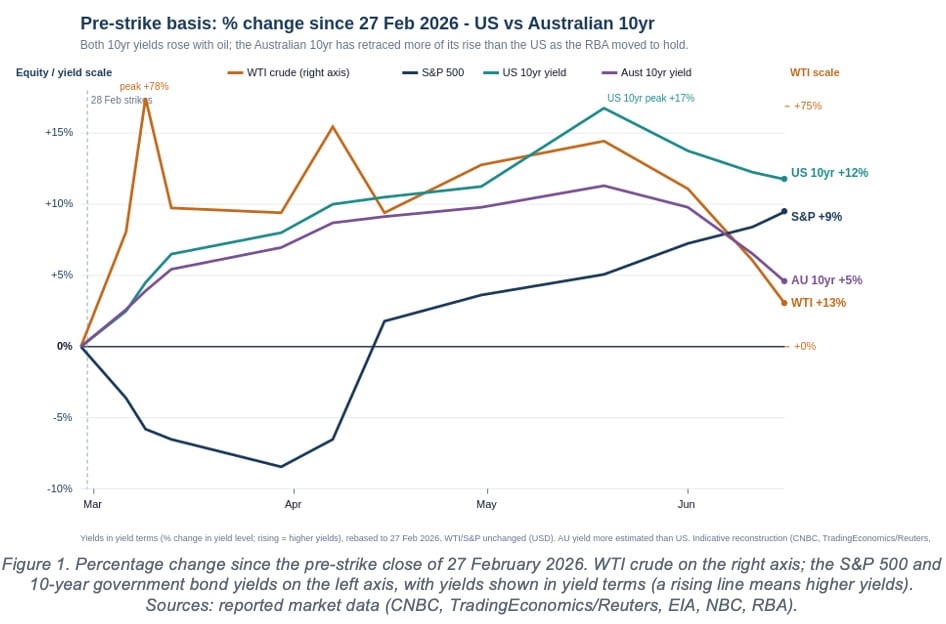

The bond market has not let go

The bond market tells the more important story, and a more cautionary one. Treasuries sold off alongside oil in the days after the war was announced and, unlike oil, they have not come back. The US 10-year yield has risen from about 4.00 per cent on the eve of the strikes to around 4.47 per cent today, an increase of approximately 47 basis points, or close to 12 per cent in yield terms. Having peaked near 4.67 per cent in May, its highest level in more than a year, the yield has retraced only a fraction of its rise. The long end has been firmer still, with the 30-year reaching 5.2 per cent in May, a level not seen since 2007.

The divergence between a normalising oil price and a bond market that remains elevated is the signal worth heeding. The oil spike was the trigger, not the cause. Yields are being held up by three more durable forces. First, ongoing concern about underlying, pent-up inflation, on which the energy shock was layered rather than being its sole source. Second, the prospect of further central bank action, with markets having shifted from pricing rate cuts at the start of the year to pricing a possible Federal Reserve hike. Third, refunding and fiscal-supply concerns, particularly in the United States, where large deficits and heavy Treasury issuance continue to lift the term premium investors demand to hold longer-dated debt. None of these eases simply because crude has fallen.

The same pattern is visible, in milder form, in Australian Commonwealth Government Bonds, where the 10-year yield rose with oil and has since retraced more of its move as the Reserve Bank shifted to hold after its earlier hikes. The implication for income investors is constructive. The yields now on offer are underpinned by structural rather than transitory factors, which makes the income they provide both real and reasonably durable. Oil has told us the war premium has deflated, and equities are pricing a benign outcome, but the bond market, the most candid of the three on inflation and fiscal risk, is declining to ratify that optimism.

")

Platform To Digitally Trade Corporate Bonds")