Key takeaways:

- Our analysis suggests UK rates could behave very differently depending on which leadership pairing emerges and whether continuity-minded fiscal management prevails.

- Bond markets are already doing much of the fiscal policing themselves. Higher long-end yields have imposed discipline before politicians have had the chance to.

- The growth tailwinds that supported the UK economy earlier this year are fading, while fiscal constraints continue to tighten. Against that backdrop, we still see scope for 10-year gilt yields to move below 4.5% over the coming year as slowing growth eventually outweighs political noise and market pricing for rate hikes this year unwinds.

Politics change, fiscal arithmetic doesn’t

Political uncertainty continues to grip the UK. Add in stretched public finances, deteriorating growth momentum and a Bank of England facing an increasingly difficult balancing act, and it is easy to see why many investors have struggled to embrace UK assets.

Yet the most notable response to Prime Minister Starmer’s resignation this week was its absence. Gilts barely budged while sterling was largely unchanged.

Investors already anticipated the likelihood of a leadership transition and are increasingly looking beyond personalities toward a more fundamental question: can any government restore confidence in the UK’s fiscal trajectory?

Fiscal credibility matters most

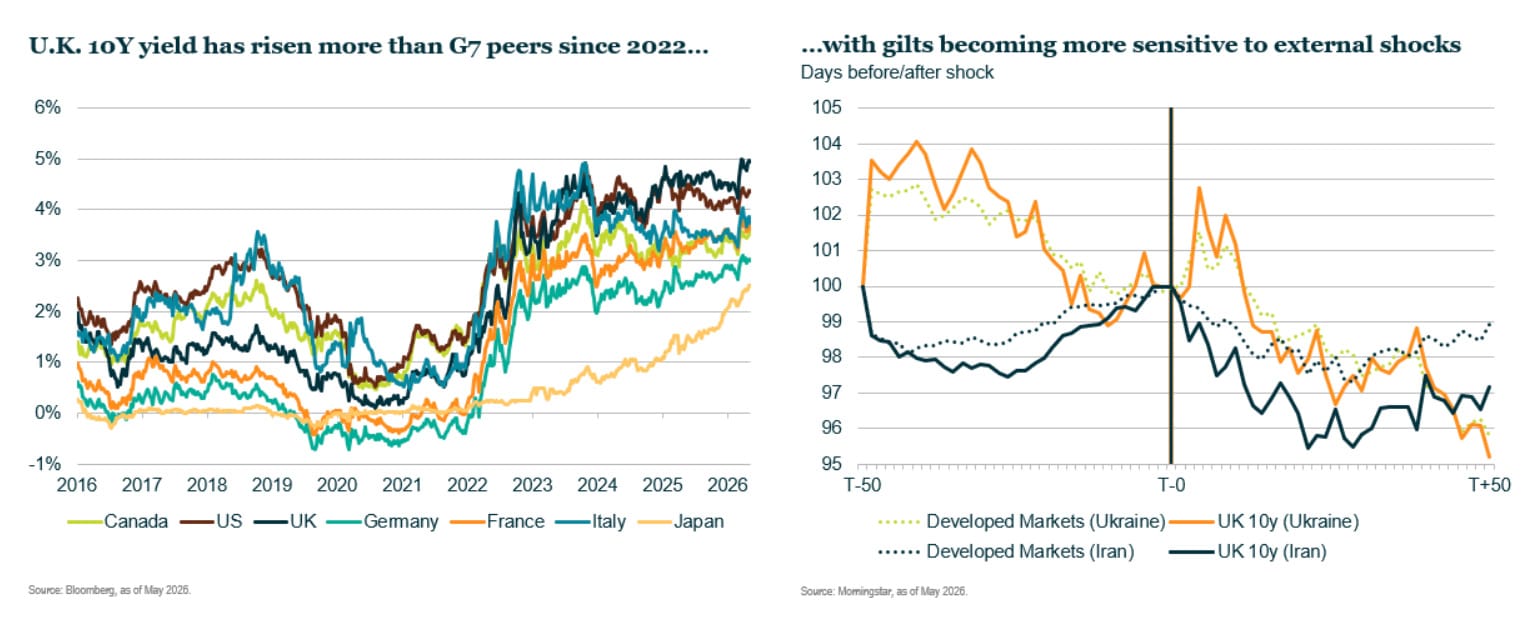

For much of the past decade, politics was itself the source of market volatility. Brexit, successive prime ministers and the 2022 mini-budget crisis all created political shocks that spilled directly into asset prices. Gilt yields subsequently still trade with an embedded risk premium and are more vulnerable to shocks than DM peers (see charts below).

But today the relationship appears to be reversing. Markets are constraining politics rather than the other way around. In many respects, Britain has become a laboratory for a world in which bond markets are once again increasingly imposing discipline on governments.

The clearest evidence comes from the behaviour of UK rates. The UK-US 10-year yield spread has compressed sharply from ~66bps in late April to around 34bps today, even as the probability of a Burnham-led government has risen materially. If markets viewed a leadership transition as inherently destabilising, we would expect the opposite.

That compression though, reflects clarity over who succeeds Starmer, not certainty over what comes next. The gap between them is where the risk now sits.

Investors appear comfortable with the idea that political change may be less disruptive than previously feared, provided the leadership uncertainty resolves quickly and in an orderly way. That does not mean markets are relaxed about the UK’s outlook. The premium has compressed on succession risk, not on policy risk, which has not yet been tested.

The challenge facing the chancellor

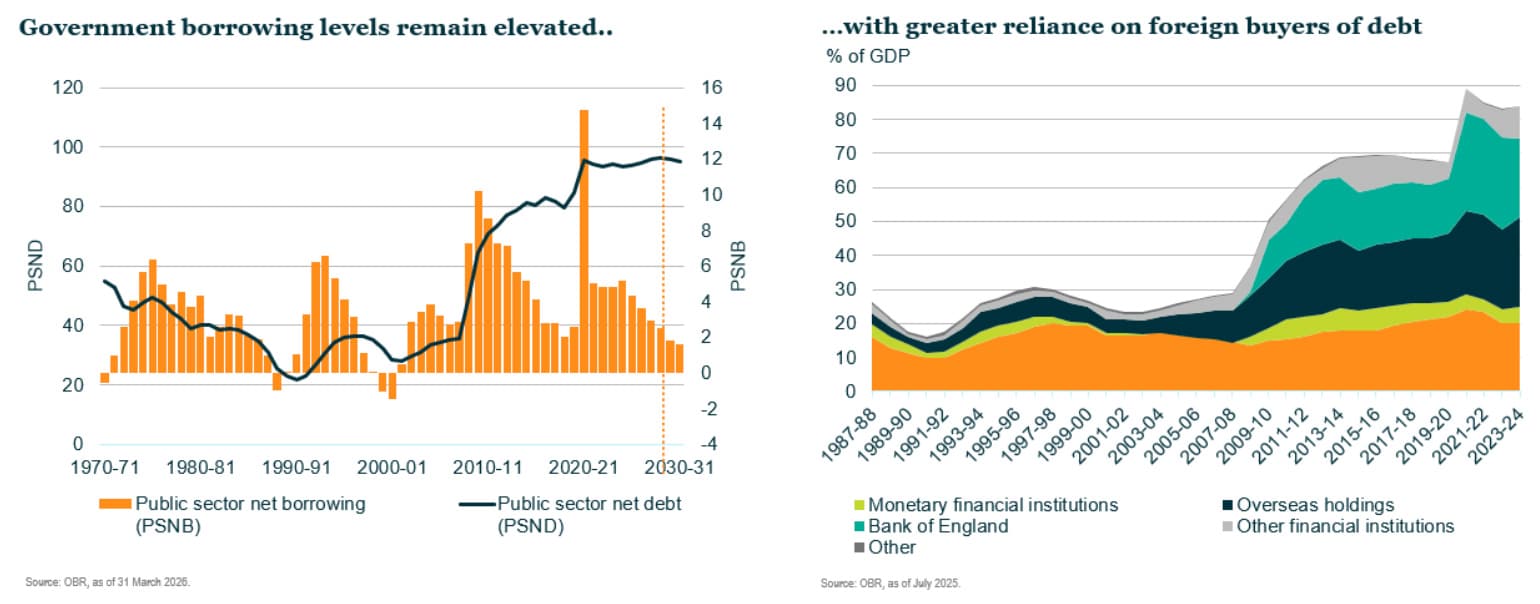

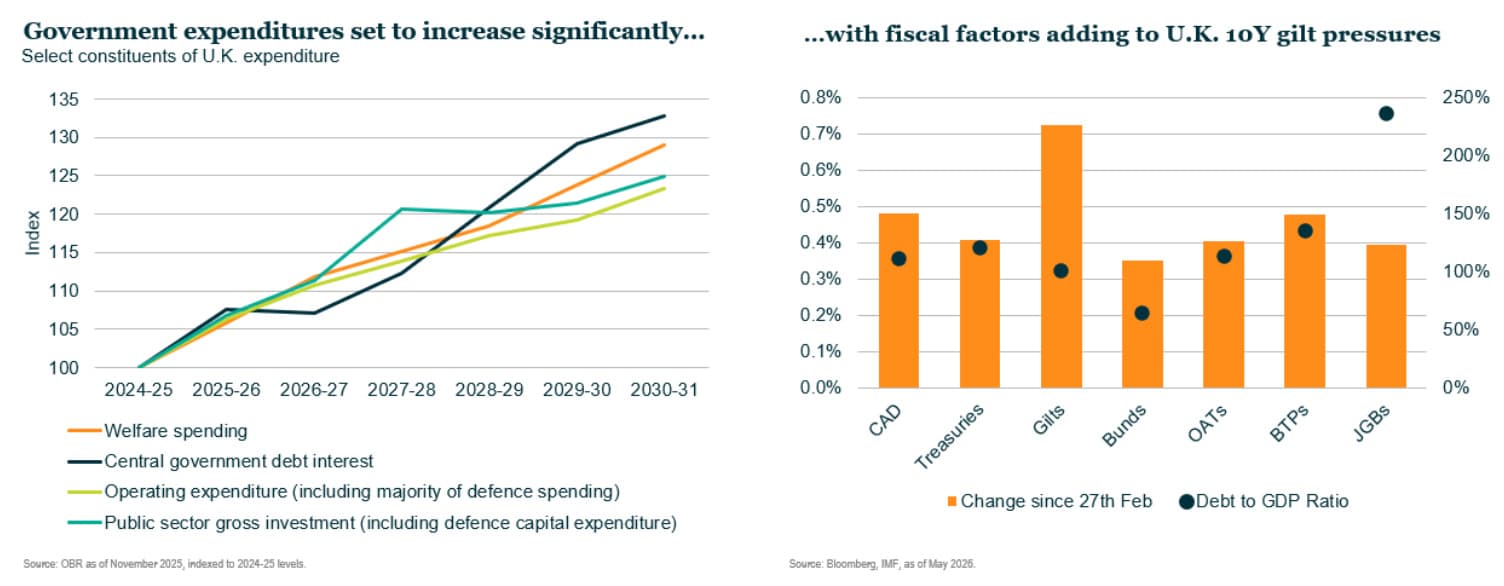

Whoever emerges as the next UK chancellor will inherit an economy with little room for error. Public debt has climbed to roughly 95% of GDP, the highest level since the early 1960s. Government borrowing is already running close to £8 billion ahead of official forecasts year-to-date, while the growth rebound seen earlier this year is beginning to fade.

Against that backdrop, investors are asking a very familiar question: will fiscal rules remain a constraint or simply a political aspiration? It is no longer whether fiscal rules survive, but whether they remain binding when growth disappoints and spending pressures intensify.

What to watch: Eleven, not ten matters most

The most important development over coming weeks may not be who occupies Number 10, but who occupies Number 11 – the Chancellor’s residence.

The combination matters as much as the individual. Our analysis suggests UK rates could behave very differently depending on which leadership pairing emerges and whether continuity-minded fiscal management prevails. Within a Burnham-led government, the chancellor appointment is the variable to watch most closely as a centrist pick would likely be read as reassuring versus a more market-skeptical outcome. The latter could drive the US-UK spread further from its 15-20bps ‘non-political baseline’.

For now, bond markets are already doing much of the fiscal policing themselves. Higher long-end yields have imposed discipline before politicians have had the chance to.

The investment implications

The recent developments do little to alter our broader medium-term view, only the path by which we get there. The growth tailwinds that supported the UK economy earlier this year are fading, while fiscal constraints continue to tighten. Against that backdrop, we still see scope for 10-year gilt yields to move below 4.5% over the coming year as slowing growth eventually outweighs political noise and market pricing for rate hikes this year unwinds.

The near-term path is less straight-line that the destination implies. Our base case is for the UK-US 10yr spread to compress further only if the succession resolves cleanly and the eventual chancellor is read as a fiscal continuity pick. The alternative would likely see some re-steepening of the gilts curve. We are not in the 2022 mini-budget territory – the post-LDI system is materially more resilient, with higher liquidity buffers, lower leverage and less vulnerability to the forced-selling dynamics that amplified the crisis – but a narrower version of that dynamic remains a live near-term risk.

Politics may continue to dominate headlines, but fiscal arithmetic remains the ultimate constraint. Bond markets have shown they can tolerate difficult fiscal dynamics for a time. But what they struggle to tolerate is the perception that credibility is being sacrificed faster than the numbers can improve – and that test, for this government, lies ahead.

[*As of 31 March 2026]

")

Platform To Digitally Trade Corporate Bonds")