The Australian fixed income landscape has changed with conditions now likely to provide many of the defensive attributes that investors have traditionally expected from the asset class, notes Anthony Kirkham, Head of Investment Management Australia at Western Asset, part of Franklin Templeton.

Kirkham says: “The Australian fixed income landscape in 2023 is very different to what it was just 12 months ago. At the onset of 2022, investors scouring the globe for yield opportunities were continuing to stretch risk and liquidity budgets in their pursuit of reasonable prospective returns.

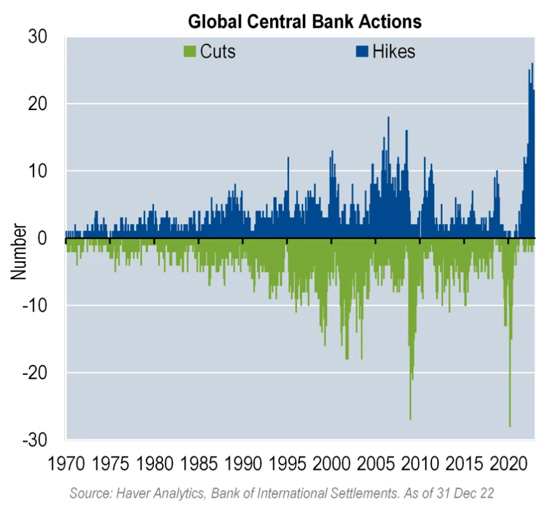

“By the end of March 2022, having peaked at US$18.4 Trillion in December 2020, negative yielding debt outstanding had fallen to US$3Trillion. In hindsight this was a preliminary sign of the conclusion of the ‘easy policy’ era. Central bankers who had driven yields to near zero or beyond to provide cheap funding and promote growth were being forced to reverse course. Then, rising inflationary pressure linked to aggressive monetary and fiscal stimulus, COVID related supply chain disruptions and energy supply shocks all combined to push inflation to record levels.

Also read: The Benefits of Global High Yield

“The war in Ukraine only exasperated these challenges on the energy and agricultural fronts and central bankers’ policy rate normalisation quickly followed suit. By the start of 2023, the balance of negative yielding debt evaporated following Japan’s unexpected policy shift and more widely, the yields on fixed income assets had hit compelling levels.

“While a huge challenge for fixed income investors, coordinated central bank actions caused a remarkable reset for the asset class. With that, the asset class’ key attractions, including high income and total return potential, diversification benefits via a low to negative correlation with growth assets, and defensive attributes linked to potential capital appreciation in times of stress, are back after a long period of rate manipulation that started post GFC.”

Kirkham adds that income and total return potential is back, especially in select credits.

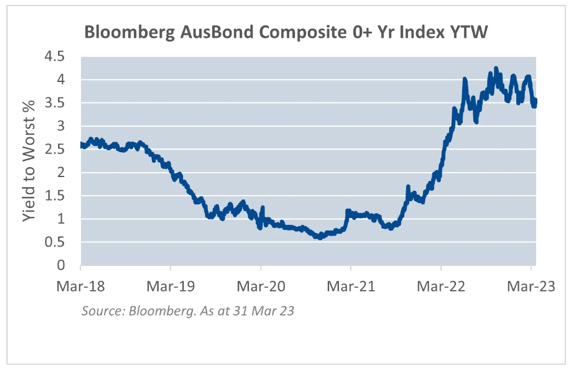

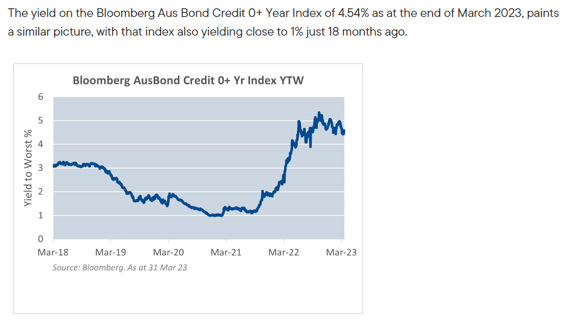

He says: “Comparing the yield on the Bloomberg AusBond Composite Index at 3.5 per cent as at the end of March, to a yield close to 1% just 18 months ago illustrates how far yields have moved in a short space of time.

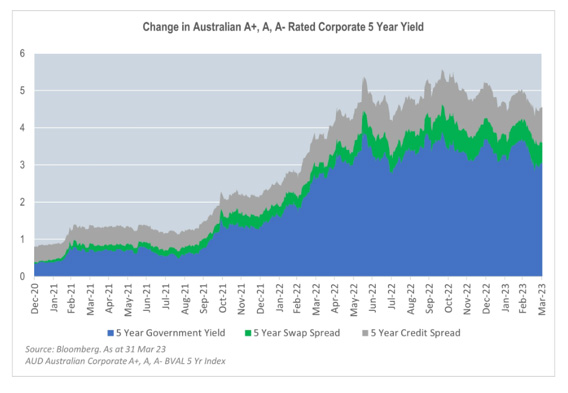

“Along with the higher rates caused by the aggressive monetary policy shift, index yields moving higher in Australia are tied to two additional factors. The first was swap spreads widening across the curve, as liquidity tightened and rate volatility impacted trading markets. The second was credit spreads widening as investors re-evaluated the earnings profile of corporates in a rising rate environment. In combination with higher yields, the path for returns was a challenge.

“In combination, these moves present fixed income investors with an opportunity to achieve higher prospective returns, without taking on additional credit or illiquidity risk. For investors in Australian fixed income and credit, the opportunity set is particularly compelling.

“Credit spreads, which represent a credit investor’s compensation for the increased risk of default above risk free government securities of equivalent terms, are trading at similar levels in Australia compared to offshore markets. This comes despite Australia boasting a relatively high-quality issuer base and a fairly unique market structure.”

Kirkham says: “Australia’s higher quality market is tied to Australian credit being dominated by investment grade issuance and a limited high yield market. Increases to the cost of capital that result from downgrades to sub-investment grade are particularly punitive in Australia. Issuers therefore are conscious of adhering to debt covenants to appease rating agencies and maintain investment grade ratings; comforting for investors.

“The unique structure of the Australian market is linked to the monopolistic and duopolistic nature of a range of industries commonly issuing into the domestic market. Especially valuable for more highly levered BBB rated issuers in the infrastructure and utility sectors, this brings about pricing power allowing inflationary pressures to be passed on to consumers.

“Identifying the businesses best placed to deal with the current economic picture and those trading below fair value requires both in-depth credit analysis and active management which we believe will prove particularly worthwhile as we move toward a likely economic contraction.”

He says: “2022 was a standout year not just for the magnitude of the moves in equity and fixed income markets but also because it reminded investors that fixed income and equity markets can decline in tandem. 2022 appears to be the exception rather than the rule as the COVID policy backdrop pushed interest rates exceptionally low and equity markets reached near all-time highs due to cheap financing and the ongoing hunt for returns.

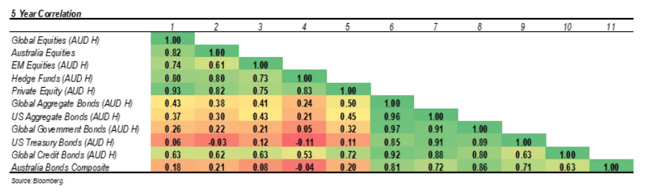

“A historical low to negative correlation between stocks and bonds is driven in part by the fundamental structure of each asset class’s cash-flows. Equity cash-flows/dividends are not contractually guaranteed and are therefore subject to the fluctuations of the business cycle. Whereas, fixed income securities’ cash flows are predetermined and contractually guaranteed.

“In times of stress, growth expectations typically fall and equity valuations follow. Customarily, market stress also causes a coincident reassessment of the path for rates, with expectations of monetary easing by central banks to promote growth causing bond prices to rally. The move higher in yields recently promotes greater capital appreciation potential in such times of stress and correlation benefits. Recent financial stability issues serve to highlight this.

“The month of March 2023 was characterised by a drastic recalibration of cash rate expectations and terminal rates for central banks off the back of financial sector concerns caused by issues at Silicon Valley Bank and subsequently Credit Suisse. Fixed income rallied strongly in that environment.”

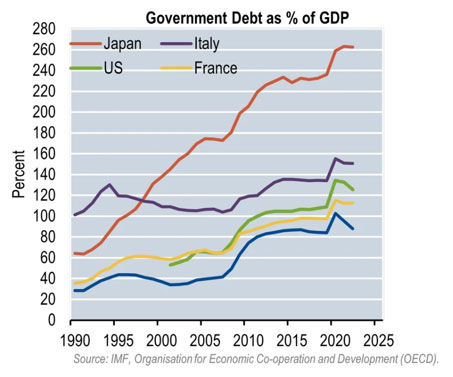

Revisiting asset allocations, Kirkham notes: “After a rapid and challenging reset, there is growing evidence to suggest that central bank actions are having their intended consequences, slowing economic growth to balance demand and supply and moderate inflation. Our analysis also indicates that the forces that preceded the recent inflation shock, including high government debt, ageing demographics and technological displacement will ultimately reassert themselves.

“With that in mind, higher yields and wider spreads offer compelling investment opportunities for fixed income investors. A combination of higher income and potential capital appreciation, matched with renewed diversification benefits and the likelihood of a more stable return profile going forward, sees the asset class well placed to deliver the attributes sought out by investors.

“Fixed income remains a critical building block for portfolio construction and investors should always consider the advantages of the differentiated cash flow characteristics offered. Investors should be encouraged to revisit their strategic allocations,” says Kirkham.

")

Platform To Digitally Trade Corporate Bonds")