Is my fund manager doing a good job?

Fund managers play an important role in the provision of secure retirements for millions of Australians. So, it is important to be able to assess a fund manager’s performance. It remains very common for market benchmarks to be used in this assessment process; for example, Australian equity managers may be assessed against the S&P/ASX 200 Accumulation Index – the more they outperform the Index, the better managers they are perceived to be.

When it comes to fixed income, this approach is problematic. In this article, we will explain why this is the case. We will then suggest alternative approaches and a practical way to gauge whether your fixed income fund manager has done a good job, or not.

Is indexing an appropriate framework?

There are many ways to define success in fixed income. The main one is outperforming a given market benchmark and, the Bloomberg Barclays Global Aggregate Index is a good example. It contains a wide variety of bonds including those issued by governments, sovereign agencies and municipalities, and corporates. Each bond is weighted by its size; which means that the largest bond issuers are those with the largest index representation.

The Bloomberg Barclays Global Aggregate Index shows the country of risk grouping noting the predominance of the United States and Japan, which are two of the largest issuers of sovereign bonds.

Issue: Too much exposure to the biggest debt issuers

This is an important flaw of benchmarks in the fixed income universe. Remember, an entity issuing a bond is, all else being equal, increasing its debt. The more bonds that a company or other bond issuer has outstanding, the greater the representation that issuer will have in an index. Thus, the United States and Japan are the largest countries represented in the Bloomberg Barclays Global Aggregate Index. We could show other indices as well and the same issue would be apparent.

Investors who follow fixed income benchmarks are often compelled to invest ever greater amounts in bonds of issuers that already have large debts outstanding, eschewing more attractive risk-adjusted expected returns elsewhere. This clearly fails the common-sense test. In fact, the optimal approach to fixed income investing leads to the exact opposite situation, where investors allocate more cautiously to entities with more debt outstanding. Why? There are two main reasons that are best illustrated by comparing bonds to equities:

- An equity manager may be rewarded for a concentrated position in few stocks. A bond manager will not. In fixed income, upside returns beyond the income expected at the initiation of the investment are limited.

- Both equity and bond investors face the total loss of capital in the event that something goes wrong.

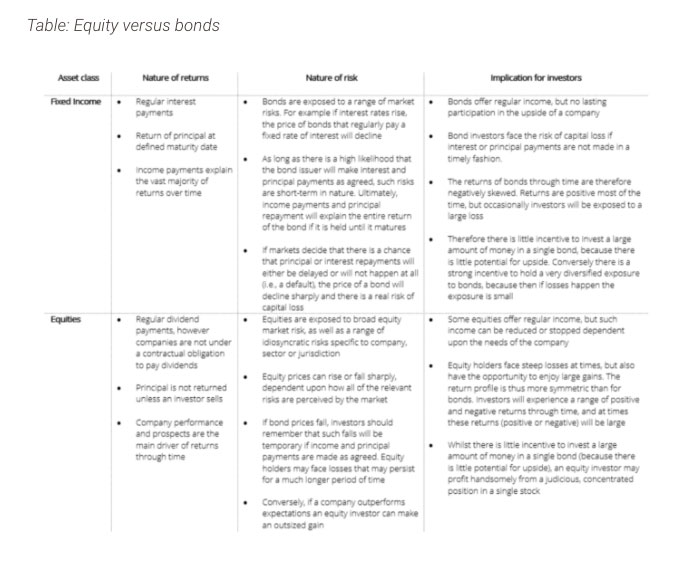

The table at the end of this paper contrasts the characteristics of bonds with those of equities more fully. For now, the main takeaway is that given the asymmetric risk profile of bonds it makes no sense to make large, concentrated bond investments.

Issue: Opportunity costs

Fixed income markets are extremely large and diverse, and are multiples of the size of equity capital markets globally.

There is a huge diversity of issuers in the bond market for investors who are sufficiently resourced and incentivised to look for good risk-adjusted returns. This illustrates another problem with indices in bond markets, indices have become less representative of the rich opportunity set available, because increasingly they have become dominated by the issuance of large bond issuers, like governments.

There is no single index that does even a reasonable job of representing the very large investable universe. That is the case locally, and even more so offshore. Thus, investors who use benchmark-focused approaches are suffering a meaningful opportunity cost. The index dictates investment decisions that should, in fact, be dictated by careful research of whether risks are being adequately compensated.

Issue: Timing of investment

In fact, investors who follow indices often incur actual costs too. Consider the decision a borrower faces when fulfilling their funding needs. Sometimes there is an imminent need that determines timing, but often the decision is based on price. That is, bonds will typically be issued when an issuer considers the cost of doing so to be low. Lower cost issuance means lower expected returns for investors and when investors bid up the price of some new issues because of likely inclusion in an index, expected returns are reduced still further.

Once a bond enters a benchmark index, this cycle of perverse behaviour can continue. Consider what an investor should do if a bond increases in price by more than similar bonds. Given our comments earlier about the significant breadth of opportunity in global fixed income markets and also the limits to upside potential in fixed income investing, common sense might dictate reducing exposure.

An appropriately directed research effort is likely to uncover another bond with a similar risk profile that offers investors a better income stream. Is this the action a benchmark-hugging investor will take? Perhaps not. In fact, such an investor may feel compelled to do the opposite, because weightings in benchmarks increase with price.

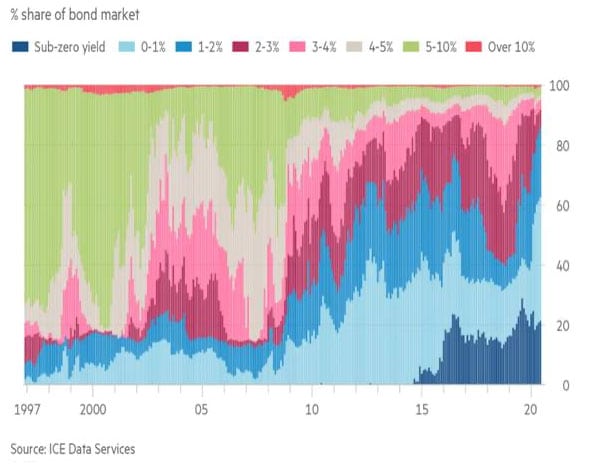

An egregious example is the massive issuance of bonds by government issuers engaged in quantitative easing. This has pushed the yields of an increasing basket of bonds into negative territory, as shown in Figure 1 below.

Outside of official demand, much of the demand for these bonds is likely to come from investment managers who are beholden to market benchmarks.

Figure 1: Stock of bonds with negative yields

Issue: Flawed manager incentives

What services should a fixed income fund manager be providing for their clients? A benchmark-focused manager aims to outperform the benchmark; is this sufficient? If an index is down 2% and a fund manager is only down 1% the fund manager will be pleased with their efforts, but will the end investor also be pleased? Investors have many different risk/return preferences, time horizons and so on; but many view losing money as a poor outcome, full stop. We believe that the strong growth of absolute return fixed income funds over time shows that this mismatch between fund manager incentives and investor expectations remains an issue among the end users of fixed income.

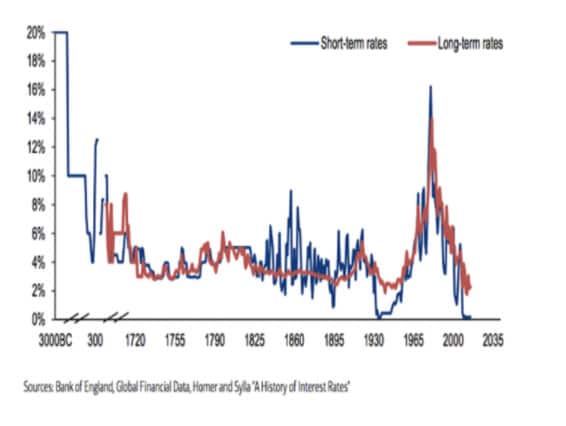

Issue: Interest rate risk

The final issue that we highlight concerns interest rate risk. Many fixed income indices are biased towards (and often exclusively focused on) fixed rate bonds. For example, the Bloomberg/Barclays Global Aggregate Index mentioned earlier has seen its duration drift from 5.3 years pre-crisis, to more than 6 years today. This is partly due to issuance patterns through time, but it is also reflective of the market environment because all else being equal, as interest rates fall the duration of fixed rate bonds increases further.

Interest rates will eventually rise both locally and globally, although this is not likely in the near-term. At the same time, it is unlikely that most interest rates will fall much further either. This leaves investors running long duration positions exposed to capital losses down the track. Another related issue is defensiveness. Index-aware investment approaches are used by many investors in large part because they expect this part of their portfolio to offset losses in their equity portfolios. Historically, duration has been the most important driver of this defensive behaviour, causing fixed rate bonds to rise in value as interest rates and equity prices fall. But with bond yields at lows not seen for literally thousands of years, bond prices do not have the same ability to rise as they once had. Of course, central banks in some jurisdictions have resorted to negative interest rates to increase the scope for bond prices to rise. Even then, however, there are greater limits to bond price appreciation now than have been the case for some time. As Figure 3 below shows, this has reduced the ability of a ‘traditional’, duration-heavy bond allocation to play the role of shock absorber in a multi-sector portfolio.

Figure 2: Interest rates are at extraordinarily low levels

Solutions

We have outlined a number of reasons why a benchmark-relative approach to fixed income is sub-optimal. Broadly, there are two courses of action investors might take as a result:

- Change the nature of the benchmark

A number of index providers have proposed changes to benchmark indices designed to address some of the issues listed above. Such approaches are commonly called ‘smart beta’ and involve altering the weighting methodology used to construct indices. In fixed income, one such change might be to weight bonds in an index according to metrics that impact issuers’ ability to repay debt. Sales, cash flow, or book value of assets are all metrics that come to mind; for example, a corporate bond benchmark may be constructed with larger weights to companies with better cash flow generation. Such a benchmark would go some way to alleviating the issue mentioned above, where traditional benchmarks shepherd investors toward debt-laden companies.

A smart beta approach represents a more logical choice than a traditional benchmark for a fixed income investor. But such an approach does nothing to address any of the other issues we highlighted. This is why we believe the best way to manage a fixed income portfolio is to remove benchmarks from the discussion entirely.

- Target an absolute return

Instead of outperforming a benchmark with minimal tracking error, success instead could be defined as delivering the targeted return in the context of specifically targeted risk exposures that are tailored to bond investors, not to an index provider’s rules that may instead advantage bond issuers. The trade-off is that the manager has full access to global fixed income markets in order to construct portfolios that fulfill these goals.

Truly active management should mean that managers are not beholden to arbitrary benchmarks. End investors are able to access a portfolio where expected returns and risk tolerances are carefully defined:

- Investments are made solely on the basis of attractive risk-adjusted expected returns. Lost opportunity costs are avoided.

- Investments are made when risk-adjusted returns make sense to the investor, not when issuance suits the needs of the issuer.

- The focus is on achievement of a risk/return target that can be entirely customised to the needs of the end investor. Interest rate risk can be reduced to appropriate levels given current market conditions. Returns are positive in absolute terms, not relative terms.

Disclaimer: Please note these are the views of the author and not necessarily the views of eInvest or Daintree Capital. This article does not take into consideration your personal needs, investment objectives or financial situation. Read the PDS at einvest.com.au

")

Platform To Digitally Trade Corporate Bonds")