By Vincent Chung, CFA Portfolio Manager at T. Rowe Price

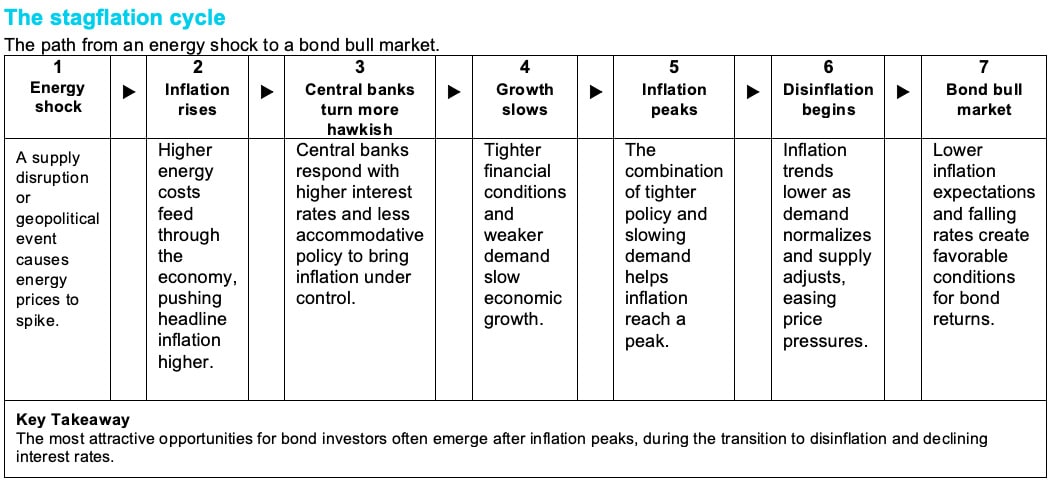

Recent tensions in the Middle East and the resulting energy supply shock have heightened investor concerns about a return of stagflation—a period of rising inflation alongside slowing economic growth. While stagflation can be challenging for traditional bond benchmarks, history suggests it is not a reason to abandon fixed income.

In fact, some of the strongest bond returns have historically followed periods of elevated inflation, as economies transition from stagflation to disinflation. The key question for investors is not whether to own bonds, but whether they own a strategy with the flexibility to navigate both phases of the cycle.

One of the biggest misconceptions about stagflation is that it affects all markets equally. History shows otherwise. The oil shocks of the 1970s created dramatically different outcomes across regions. Energy-importing economies such as the UK experienced surging inflation, weaker growth, and poor bond returns, while commodity-producing economies generally proved more resilient.

Similar patterns emerged following the Iranian Revolution in 1979 and during the inflation shock of 2021 to 2022, when Europe was more exposed to rising energy prices than the U.S. and several emerging markets benefited from having tightened policy earlier.

As inflation surged in 2022 and central banks aggressively tightened policy, bond yields rose sharply, credit spreads widened and most fixed income sectors experienced significant drawdowns, with longer-duration assets hit hardest.

The recovery that followed in 2023 was equally instructive. As inflation moderated and markets began pricing the end of tightening cycles, fixed income sectors rebounded strongly. The episode highlights an important lesson: inflation shocks can create short-term pain, but they are often followed by attractive fixed income returns.

It also demonstrated the value of flexibility. A strategy able to reduce duration and allocate to break-even inflation would likely have been more resilient during the drawdown, while retaining the flexibility to add duration and potentially capture the subsequent recovery as inflation peaked and disinflation emerged.

While 2022 is the closest historical comparison to today’s environment, there are some important differences. Most notably, investors are starting from significantly higher bond yield levels. Higher carry does not eliminate volatility, but it can provide a larger income cushion against rising yields and improve prospective return potential relative to the starting point investors faced in 2022.

“While stagflationary shocks can create short-term pain, history shows they are often followed by periods of strong fixed income returns. As inflation peaks and markets begin pricing policy easing, bond markets have historically entered powerful recovery phases. Investors who reduce bond allocations during periods of peak inflation risk missing some of the most attractive opportunities in fixed income.”

Why a diversified income bond strategy is well positioned

A diversified fixed income strategy that can invest across a broad global opportunity set including sovereign bonds, investment-grade credit, high yield bonds, emerging market debt, securitized assets, currencies, and inflation‑linked securities can be particularly valuable during periods of stagflation. If an Iran‑related energy shock pushes inflation expectations higher while simultaneously weakening growth, a diversified strategy can actively adjust duration exposure, reposition across regions, sectors, and issuers, and seek opportunities where markets may be mispricing inflation risks.

Importantly, diversified strategies can reduce duration, increase exposure to break-even inflation and reposition across regions, sectors, and issuers as conditions evolve.

Stagflation is not our base case, but it is a credible risk scenario if an extended Iran‑related conflict leads to a sustained energy shock. For now, the more likely outcome is slower growth and pockets of sticky inflation rather than a broad‑based repeat of the 1970s. Importantly, U.S. growth momentum remains relatively resilient, helping to reduce the likelihood of a severe stagflationary outcome. The key indicators to watch are energy prices, inflation expectations, wage growth, and whether central banks are forced to adopt a more hawkish stance in response to persistent inflation pressures.

Another important differentiator is central bank credibility. Countries where central banks have a strong track record of controlling inflation are often better positioned in stagflationary environments. While policymakers in these countries may need to raise rates earlier and more aggressively in response to an inflation shock, they typically do not need to tighten as much overall because inflation expectations remain better anchored. The experience of the 1970s illustrates this point. Germany’s Bundesbank was generally more proactive in responding to inflation pressures than many of its peers, helping to preserve policy credibility and ultimately limiting the scale of tightening required relative to countries where inflation became more deeply embedded.

Regional vulnerability to a stagflation shock

Higher Vulnerability: UK and Europe Most exposed due to imported energy dependence, weaker growth prospects, and greater sensitivity to higher commodity prices.

Lower Vulnerability: United States Stronger growth momentum and domestic energy production may help provide insulation, although a prolonged energy shock could keep inflation elevated and force a more hawkish policy stance.

Mixed Outlook: Asia Japan remains vulnerable due to its dependence on imported energy and inflation that is already elevated relative to its historical experience. China presents a more nuanced picture. Weak domestic demand and excess industrial capacity remain disinflationary forces, although efforts to reduce destructive price competition and improve corporate profitability could eventually allow Chinese producers to pass through more cost pressures, potentially exporting inflation rather than suppressing it. More broadly, many Asian economies responded earlier to the post pandemic inflation shock than developed markets, leaving the region generally better positioned to absorb a renewed energy-driven inflation impulse.

Rest of World Commodity exporters such as Canada and parts of Latin America could benefit from stronger terms of trade and higher commodity revenues. Meanwhile, countries such as Brazil and Mexico entered this period with higher real yields and greater policy flexibility after tightening aggressively earlier in the inflation cycle.

Stagflation should not be a reason to abandon fixed income.

Periods of stagflation can be uncomfortable for investors, but they should not be a reason to abandon fixed income. History shows that inflation shocks can create significant divergences across regions, sectors, and asset classes, generating opportunities for active managers with the flexibility to respond.

More importantly, stagflation has historically been a transition phase rather than a permanent state. As inflation eventually moderates and growth slows, bond markets have often entered a disinflationary environment that has been supportive of fixed income returns.

The investment implication is clear: rather than reducing bond allocations, investors should consider whether their fixed income exposure is flexible enough to navigate both the inflationary shock and the disinflationary recovery that often follows. The Diversified Income Bond Strategy managed by T. Rowe Price was designed with precisely this objective in mind.

")

Platform To Digitally Trade Corporate Bonds")