")

Not so long ago, sovereign rates were fairly stable and of little concern to investors, but fiscal spending to assist during the pandemic and the fuel crisis has sent government debt to GDP worryingly higher. Sovereign risk and government bond rates are again front of mind and showing significant volatility.

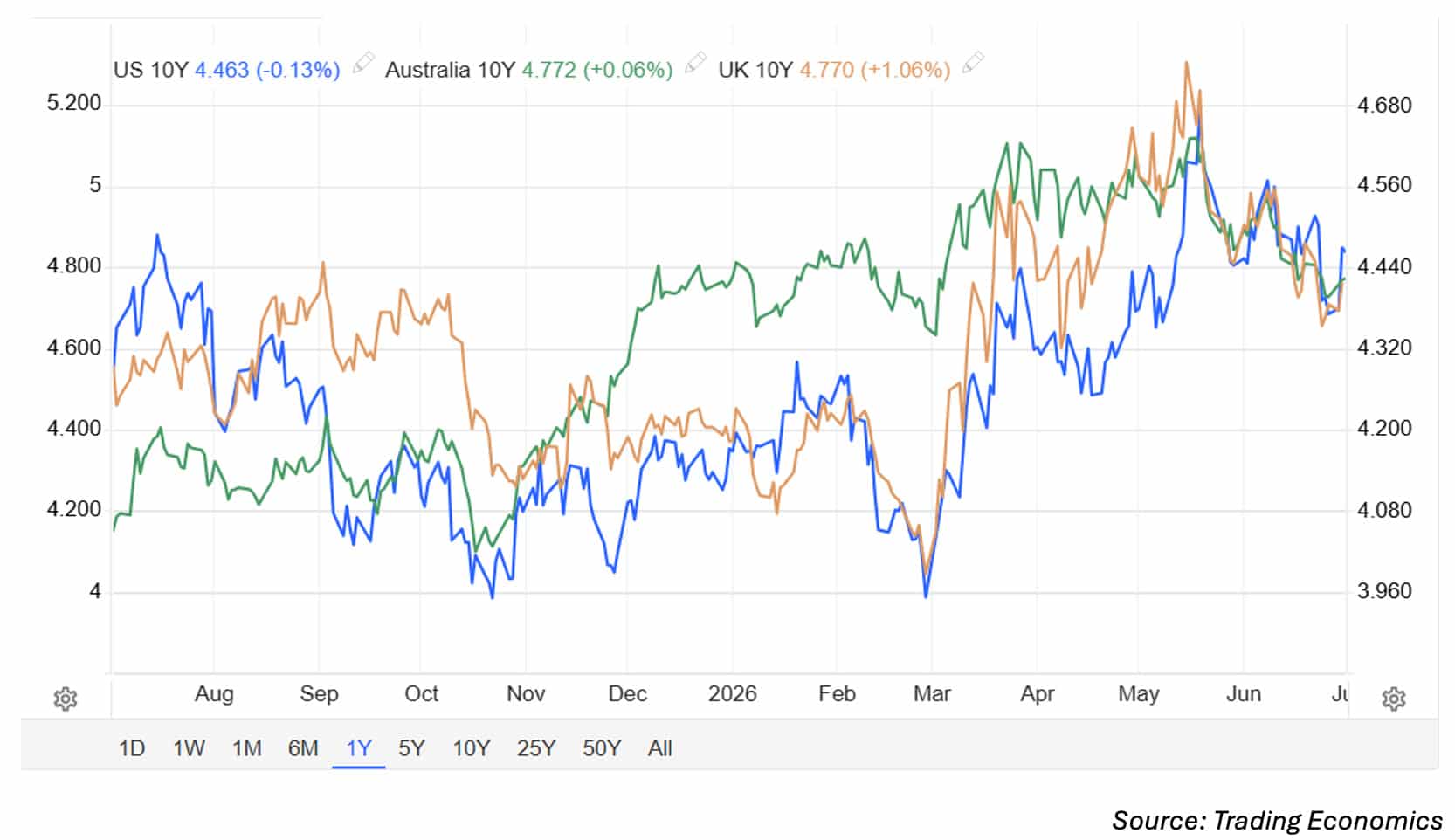

The graph below shows the US, Australia and UK 10Y government bond yields over the last 12 months. The UK and US are particularly volatile. The UK low was 4% in March and peak in May at 5.34%.

Both the Australian and UK 10 year government bond rates are 4.77% as of 30 June 2026 (see the green and orange lines below) and the US (in blue) is 4.46%.

US, Australia and UK One Year, 10Y Government Bond Yields

When you can get a capital-protected income of close to 5%, you need to reassess the risk premium you are being offered on other investments. Many are trading at margin lows as Alex Veroude from Janus Henderson points out in his excellent contribution on ‘Putting things into Perspective’.

I found the assessment of the UK economy and its sovereign yields from Laura Cooper of Nuveen particularly insightful. The bond market is helping keep government spending in check.

Adam Marden from T. Rowe Price argues a more data dependent US Fed coupled with reduced forward guidance should translate to higher rates volatility.

Chris Iggo from BNP Paribas typically has some useful observations to make and in this week’s article, he says, any new adjustment to interest rate levels will hit fixed income returns in the short term and may undermine equity valuations. Iggo generally views bond and equity markets favourably, but considers what could go wrong.

Finally, Andy Armstrong from Challenger Investment Management discusses the need to sit down with private credit teams and that remote data analysis is insufficient. He outlines what he’s looking for.

In Australian corporate bond market news:

- Bank of Queensland is taking indications of interest for a floating rate 10 non-call five (10NC5) subordinated bond with price guidance of 175 basis points over 3-month BBSW

- CBA is taking indications of interest for a floating and/ or fixed rate five-year senior deal with price guidance of 73 basis points over 3-month BBSW

Have a great week.

")

")

Platform To Digitally Trade Corporate Bonds")

")